Why Despegar.com Inventory Is A Maintain Amid Market Challenges (NYSE:DESP)

Summary Aerial Artwork

Despegar.com, Corp. (NYSE:DESP), much like Reserving Holdings (BKNG) however primarily in Latin America, has a enterprise mannequin of intermediating the sale of tourism companies, incomes commissions for doing so. The corporate has succeeded in gaining a important share in nations comparable to Brazil and Mexico, which might be thought of certainly one of its differentials.

Regardless of this, this market is clearly nonetheless very aggressive, not solely between the completely different gamers attempting to consolidate themselves and preventing and attempting to distinguish themselves on who can supply the perfect platform for vacationers, but additionally preventing over costs and number of accommodations and locations, but additionally between the airline or resort web sites themselves, which might enhance their margin by providing their service on to the buyer.

This makes Despegar a strong firm in Latin America, however one which definitely has restricted aggressive benefits, even when in comparison with others in its sector, comparable to Reserving itself or Airbnb (ABNB), which presents a comparatively completely different service.

Though it is an organization primarily uncovered to Latin American nations, its valuation is okay however is not that undervalued, which, coupled with excessive exterior dangers, justifies my discouragement with Despegar Shares.

Despegar Delivers Some Stable Outcomes

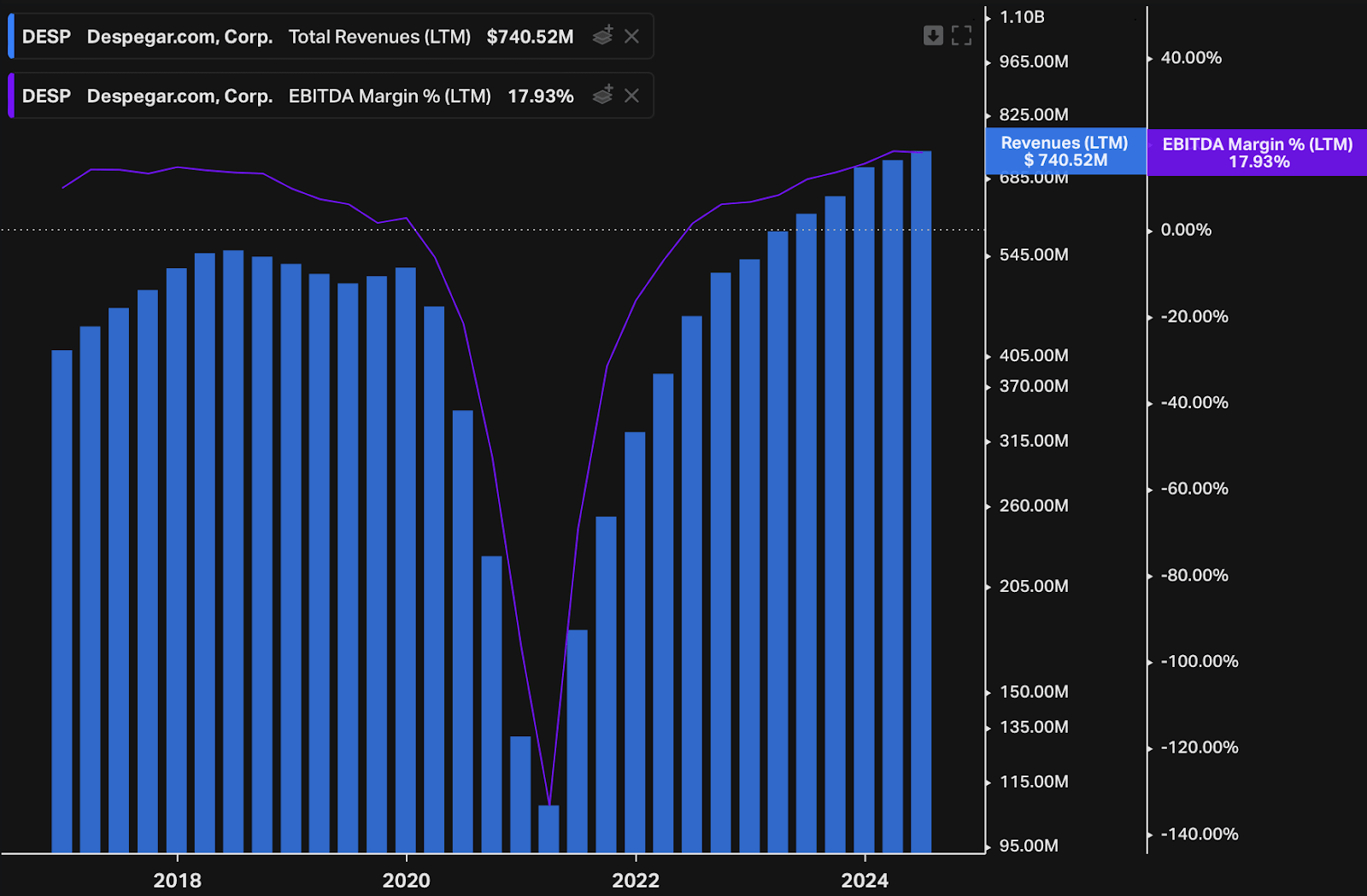

Attempting to investigate it in isolation (with out contemplating its sector an excessive amount of), Despegar is an fascinating firm that has managed to realize some success. After the cruel impacts of the pandemic, the corporate’s internet income has resumed its development and even after that, it appears to be like like it can keep an fascinating tempo of development (given its steering of no less than 8% income development for 2024). This got here along with a very good enchancment in EBITDA margin, which reached ˜20% in Q2 2024 in opposition to one thing near 12% in Q2 2023 even after larger funding and advertising bills.

Koyfin

Despegar or “Decolar,” which is the title of the model working in Brazil, sells primarily in B2C, which represents 83% of its income (and greater than 60% of that comes from Brazil and Mexico). As the corporate itself mentions, its principal market (B2C in LatAm) is extremely fragmented however nonetheless permits for development near low double digits. As well as, the corporate operates in B2B by 15,000 offline businesses, representing 9% of income, and the remaining 8% is for B2B2C, by white-label partnerships with banking functions and the like.

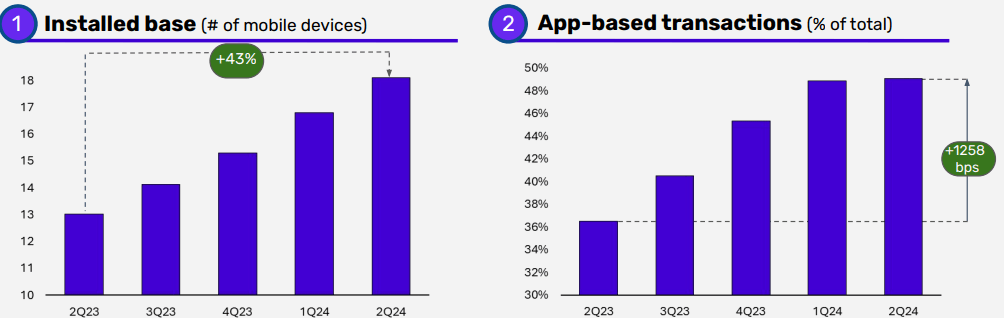

In latest quarters, the corporate has finished a very good job of accelerating its app customers and in-app transactions, at present holding the highest place in LatAm among the many hottest journey apps. In Q2, the corporate grew its put in base by 43% YoY, reaching 18 million cell gadgets, with app-based transactions reaching ATH of 49%.

Despegar 2Q24 Presentation

Though a good portion of customers nonetheless use web sites and different methods to purchase their journey, having a excessive put in base is essential and may also help construct or solidify your aggressive benefits, by growing recurrence, triggering notifications or simply being extra handy for the consumer to open the app and purchase from anyplace.

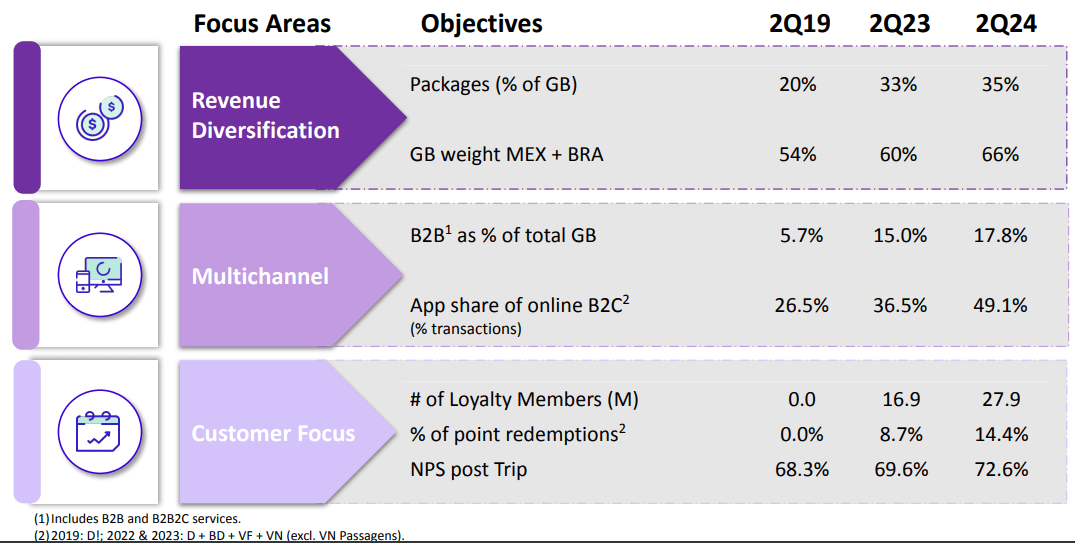

Different operational metrics have additionally proved fairly fascinating over the previous couple of years. The corporate has managed to extend the variety of packages offered, from 20% in 2019 to 35% in 2024. B2B (together with B2B2C) has additionally gained a number of illustration and is now nearly 18%. The variety of Loyalty Members has additionally exceeded 27 million, which is sweet for the imaginative and prescient of resilience and recurrence.

Despegar 2Q24 Presentation

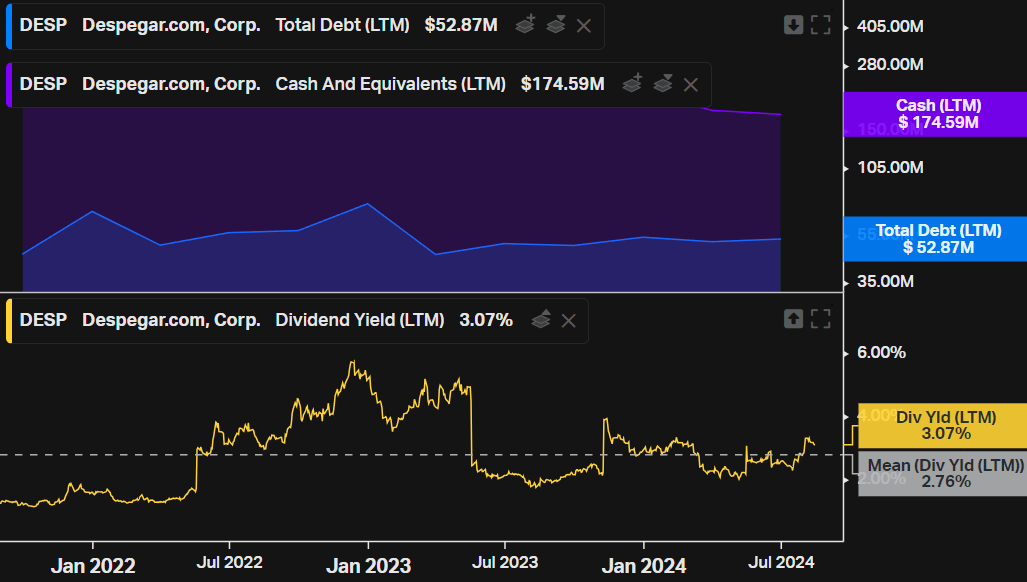

Despegar’s capital construction can also be comfy, with money and equivalents exceeding $170 million whereas whole debt is $52.8 million, permitting the corporate to distribute a part of its money within the type of fascinating dividends though it’s a growth-focused firm.

Koyfin

Dynamic Market Provides Uncertainty to Despegar’s Future

So Despegar is an efficient firm with strong fundamentals and fascinating prospects. The issue is that its market generates a number of uncertainty concerning the sustainability of those prospects over the approaching a long time.

I do not imagine that the tourism intermediation market is totally Winner-Takes-All, nevertheless it does have Winner-Takes-Most traits. On the one hand, there’s a very fragmented provide of tourism companies, with a whole lot of vacation spot choices, and in these, a excessive variety of comparable resort and lodging choices, which in flip are capable of negotiate with a number of intermediaries on the identical time, that means that there’s provide for multiple participant. However there’s a robust community impact (and Reserving is the perfect instance of this), and as soon as you’ve got constructed up consciousness of your model and accommodations, it is simpler to draw new clients and likewise new lodging. This goes hand in hand with positive factors in scale and bargaining energy, to not point out different elements which can be simply as related right this moment, comparable to the info collected from customers that enable for a excessive diploma of personalization. This all advantages the largest participant within the section and makes it extra doubtless that it’s going to proceed to realize market share on prime of this.

On the optimistic aspect, since Despegar is among the many leaders in LatAm, it may possibly proceed to profit from the dynamics of the sector to additional consolidate itself on this area. For instance, after the bust of 123milhas – an organization that some mentioned was a Ponzi scheme – Despegar managed to seize market share positive factors within the Brazilian Market. The fragility of CVC, a Brazilian firm within the sector that made a internet lack of R$22 million in 2Q24 and has a internet debt of R$836,3 million contemplating the anticipation of receivables, may additionally have helped/proceed to assist Despegar strengthen in Brazil.

In response to the January 2024 info supplied by Conversion, LATAM (airline) was the corporate with the very best Share of Search within the Tourism sector in Brazil, with 14.5%, and Despegar was in second place with 12.7%, adopted by Reserving and fourth place was CVC. When it comes to consolidated Share of Site visitors, Reserving leads with 15.8% and Decolar is in seventh place with 6.1%.

This exhibits that though Decolar may be very current within the Brazilian market and in Latin America normally (particularly Mexico), the market remains to be fairly fragmented, with different corporations providing very comparable companies.

In different phrases, whereas Despegar is certainly a dominant participant in LatAm, it additionally faces competitors from native gamers, apps/websites from first events, and (much more threatening) world gamers like Reserving. All this makes the outlook for the subsequent few years relatively murky, so even when the corporate has fascinating steering and strong outcomes, the thesis finally ends up being intrinsically riskier, and one of many premises for investing is to imagine that it’s going to not solely be capable of stay related on this market within the quick and medium time period but additionally that it is going to be capable of enhance its market share on this dynamic market.

Despegar Affords Worth however Faces Dangers

In view of this better threat, the consequence is to demand a better low cost on the shares as a way to make investments with the best doable margin of security.

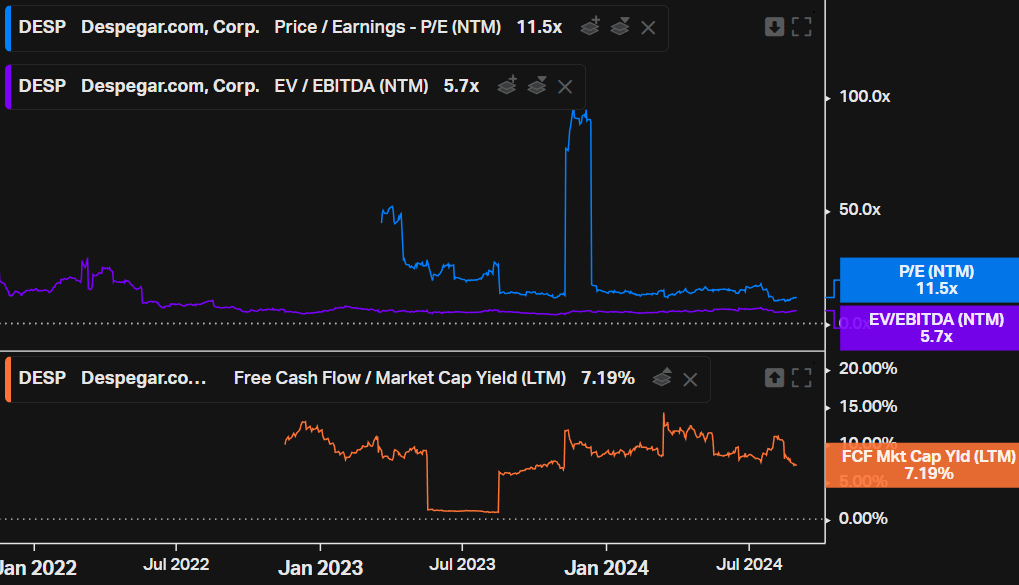

For a development firm that has fascinating development avenues, with the market projecting EBIT development of ~30% for 2024, and prospects of sustaining low double-digit development within the prime line and backside line within the coming years, Despegar is an undervalued firm. Its ahead price-to-earnings is 11.5x, whereas its ahead EV-to-EBITDA is 5.7x. Its free money movement yield can also be excessive, near 7%.

Koyfin

However we should keep in mind not solely the chance of its market but additionally the macroeconomic threat for the reason that firm is principally uncovered to the Brazilian and Mexican currencies. Nevertheless, in comparison with different Brazilian options, Despegar does not appear so undervalued. Attempting to select an choice centered on tech and development, Inter (INTR), which is a whole Brazilian digital financial institution with very promising prospects for internet revenue, is buying and selling at 14.8x its earnings for the subsequent 12 months. As for the market indices, the Brazilian index, EWZ, is buying and selling at ~8.8x, and the Mexican index, EWW, at ~7.7x.

In different phrases, the Despegar Shares at right this moment’s costs might be thought of engaging, since with this development, it is going to be doable to remunerate the shareholder properly. Even so, I do not suppose that at these multiples the shares might be thought of a discount, for the reason that macroeconomic and sectoral dangers are nice and unsure, requiring a better premium whereas there is no such thing as a moat or better consolidation within the thesis.

Closing Ideas

As I discussed, Despegar just isn’t a foul firm and has some potential by the consolidation of markets in Latin America and the dilution of prices and SG&A by better positive factors in scale. And all this at a really cheap valuation (though not that engaging), which ought to enable for a very good return for shareholders if every little thing goes based on plan in the long run.

The issue with the thesis is one thing structural. This sector is a foul one (with uncommon exceptions for the leaders and/or gamers who’re already properly established and who handle to get higher situations, comparable to Reserving Holdings), not solely due to its cyclicality and low margins, but additionally due to the uncertainty as as to whether Despegar will nonetheless be a related participant within the coming a long time, and though this threat of full disruption just isn’t so doubtless, it appears to be too excessive a threat to take (no less than at present costs and situations).