Past Meat Chapter Danger Rises (NASDAQ:BYND)

Guido Mieth/DigitalVision through Getty Photos

Over the past yr, one of many worst performing shares available in the market has been Past Meat (NASDAQ:BYND). The plant-based meat firm has seen its shares lose greater than half of their worth as income development troubles have continued. With the corporate persevering with to lose massive sums of cash, the weak steadiness sheet has this identify getting nearer to the brink.

Earlier protection of the inventory

It was a bit greater than three months in the past after I coated the identify at its first quarter report. At the moment, the corporate had simply missed income estimates for the interval, whereas giving weak steering for Q2. Regardless of persevering with to attract down on its stock steadiness, money burn continued at an alarming charge, placing working capital at its lowest level in a number of years.

With that article, I continued to reiterate a promote score on the inventory. The corporate had a really small money steadiness as in comparison with its massive debt pile, and even an open fairness sale program would not be sufficient to shut the hole earlier than the 2027 debt maturity date hit. With an unappetizing valuation, I figured both shares would go decrease on their very own, or administration would wish to dilute buyers fairly considerably simply to maintain issues right here going.

The Q2 report

Final week, Past Meat introduced its second quarter outcomes. The corporate reported revenues of $93.2 million, which did beat considerably lowered road estimates because of that weak steering talked about above. Nevertheless, the gross sales determine was nonetheless down by practically 9% over the prior yr interval, with US revenues down nearly 10% because of a virtually 19% drop within the foodservice phase. Total, the amount of merchandise bought was down by 15% over Q2 2024, however the firm was capable of elevate costs a bit to maintain the income decline within the single digits, share clever.

As the corporate works on its manufacturing plan and stock balances, gross margins did soar to 14.7%, as in comparison with simply 2.2% within the yr in the past interval. Administration has additionally introduced down working bills reasonably properly, leading to an working lack of $34 million within the interval, a virtually $20 million yr over yr enchancment. Nevertheless, that also implies that operations are shedding greater than 36 cents for each greenback of income generated, which isn’t a sustainable enterprise mannequin.

In relation to steering for the yr, the income forecast vary was narrowed from $315 million to $345 million to $320 million to $340 million, with no quantity given for the present interval. Administration trimmed its gross margin forecast from the mid to excessive teenagers to simply the mid-teens, whereas mountaineering the underside finish of its working expense forecast by $10 million, and trimming its capital expenditures forecast by $5 million on the high finish of the earlier vary.

The steadiness sheet weakens additional

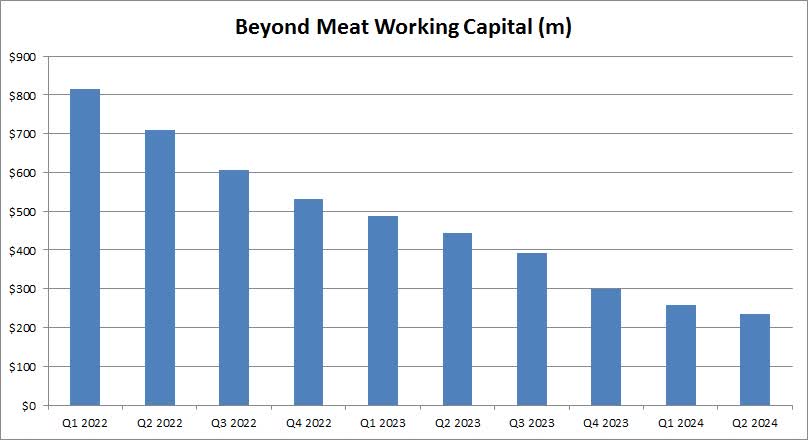

With the corporate persevering with to report massive web losses, the monetary scenario is just getting worse. Money on the steadiness sheet declined from $158 million on the finish of Q1 to lower than $145 million on the finish of June. Because the chart under exhibits, total working capital continues to return down quarter after quarter. The top of Q2 determine was simply $234 million, which was nearly halved previously twelve months.

Past Meat Working Capital (Firm Filings)

The corporate has $1.15 billion in principal debt coming due in simply over 2.5 years, a borrowing it can not pay again at this second. For the reason that conversion worth on the notes is a number of instances what the inventory at present trades for, an fairness swap will not be seemingly at this level. Administration continues to say that it’s working to deal with this main monetary downside, however it additionally hasn’t but bought any shares beneath its $200 million fairness gross sales plan, both.

With a market cap of nearly $400 million right this moment, there aren’t plenty of good choices right here. Promoting shares will closely dilute buyers, and that will not even come near plugging the debt deficit. On the identical time, even refinancing say $500 million of the borrowing would possibly end in a brand new rate of interest that might be 10% or extra, whereas the present notes pay no coupon curiosity. Including tens of thousands and thousands of {dollars} in yearly curiosity bills would make the web loss and money burn scenario even worse within the close to time period.

Valuation simply would not work right here

As of final Friday’s shut, Past Meat shares have been buying and selling for 1.2 instances their anticipated gross sales for 2025. If we take a look at another bigger gamers, Tyson Meals (TSN) went for simply 0.41 instances its anticipated revenues for its September 2025 fiscal yr, whereas Hormel Meals (HRL) went for 1.42 instances its October 2025 fiscal yr anticipated revenues. It is laborious to argue buyers ought to pay above the common of these two names for Past Meat, when you may simply spend money on these different two extra steady corporations.

As for the road, analysts noticed this identify as price $5.28 going into this week. That quantity represented appreciable draw back from final week’s end, and analysts have reduce their common by practically 50% over the previous yr. The road common peaked about 5 years in the past at round $165, just a bit whereas after shares had surged previous $230 a share, however it has been all downhill ever since.

Ultimate ideas and suggestion

In the long run, one other blended report from Past Meat has put much more strain on the corporate’s long-term future. Revenues did beat considerably lowered estimates, however nonetheless dropped over the prior yr interval. Administration was capable of present stable margin and expense enchancment, however losses and money burn stay fairly excessive. The steadiness sheet continues to weaken by the quarter, with the 2027 debt mountain remaining the most important challenge right here.

With a serious restructuring wanted for this firm, I’m persevering with to charge the inventory a promote right this moment. Both administration goes to need to dilute buyers considerably simply to stay afloat, or it might want to get plenty of assist from collectors to keep away from submitting chapter within the subsequent few years. Whereas the corporate could possibly work with lenders to get its debt steadiness down, it seemingly will end in curiosity bills that can solely make the close to time period scenario worse. On daily basis that goes by seemingly will increase the possibilities of chapter, which may wipe out fairness holders fully.