Above The Noise: Getting Again To Regular

cemagraphics

By Brian Levitt, International Market Strategist

I am declaring an finish to the COVID-19 surroundings. Daring remark, proper? Admittedly, it appears like a lifetime in the past that we had been dwelling in quarantine, however the ramifications of the pandemic have endured. Such is life when policymakers flood the world financial system with cash at exactly the second that companies are chopping staff and slashing inventories. That is not a criticism of policymakers. I imagine that true world calamity was averted. Nonetheless, inflation, coverage tightening, and fears of recession adopted. Some pundits even posited {that a} new period of inflation – and even worse, stagflation – was upon us. It was solely earlier this month when a outstanding financial institution govt warned that rates of interest had been going to 7%. Or increased! Because the gamblers may say, I will take the underneath.

My view was reaffirmed with the 2.75% annual change within the core Private Consumption Expenditures Value Index in Might.1 That is worth stability in my e-book and inside what I’ve at all times perceived to be the Federal Reserve‘s “consolation zone.” It additionally means that the present 5.25%‒5.50% federal funds goal2 is probably going too tight for the inflation surroundings. An easing cycle seems to be forthcoming, and with it, I anticipate the normalization of the US Treasury yield curve, following 19 months of inversion.3 Normalization is the operative phrase, even when it has been eons since I final shoved a cotton swab into my mind.

It could be affirmation bias, however…

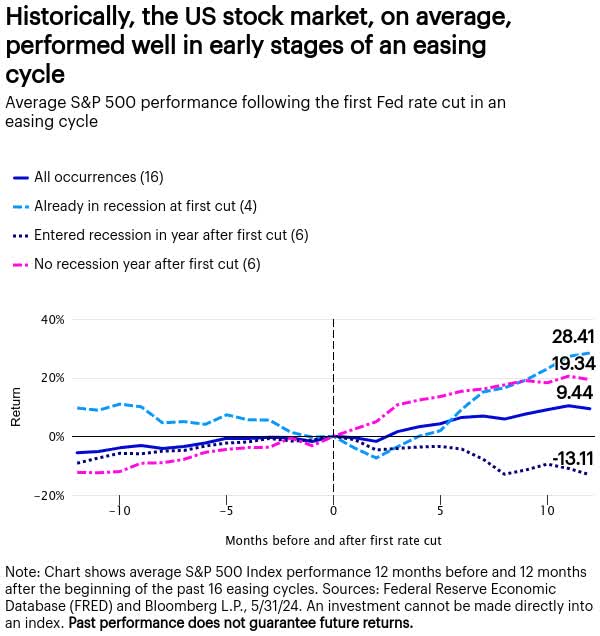

…the US inventory market, on common, has traditionally carried out properly within the early phases of a Fed easing cycle.4 That’s, if the financial system is already in a recession earlier than the easing cycle commences or if no recession happens. Easing cycles that predate recessions have been much less conducive to buyers. I suppose that is nonetheless a risk, nevertheless our most popular recession indicators, together with company bond spreads5 and financial institution lending requirements,6 aren’t flashing recession warning indicators.

It was stated

“I believe we will see the S&P go down 86% from the highest, and the Nasdaq 92%.”

-Economist Harry Dent7

A good friend as soon as informed me to make outlandish feedback to make headlines. It is by no means been my purpose to make headlines. Personally, I would like buyers to stay above the noise in order that their feelings haven’t got them deviating from their funding plans.

Harry Dent definitely made information together with his remark earlier this month. I’ve even been requested if I give credence to his views. My response is that I put as a lot credibility on this remark as I did when Dent predicted a protracted Nice Melancholy beginning in 2009 and a plummeting of the Dow Jones Industrial Common starting in 2012. Additionally, keep in mind Dent’s spending wave idea? It was the concept child boomers would sharply scale back their spending between the ages of 48 and 63, leading to excessive monetary market duress. Take it from somebody who’s 48 and elevating two teenage daughters that the spending wave idea is, as President Biden may say, “malarkey.”

Telephone a good friend

I’ve obtained plenty of questions in regards to the future independence of the US Federal Reserve. Allies of former President Trump have circulated a 10-page doc outlining a imaginative and prescient for the central financial institution that included the president being consulted on financial coverage selections. A perceived lack of financial coverage independence might have important penalties for US charges and the US greenback.

I requested Jen Flitton, Head of US Authorities Affairs at Invesco, to opine. Her response:

“The system is structured to make it very troublesome to disrupt the Fed’s independence. Any formal modifications to the operations and/or independence of the US Federal Reserve would require Congressional approval to amend the Federal Reserve Act. Such a change to the statute would want 60 votes within the Senate, an exceedingly excessive hurdle. Even when the Republicans win the trifecta in November, which means the presidential election in addition to victories within the Home and Senate, they won’t have the get together line votes within the Senate to make any important modifications to how the Fed operates.

That stated, you solely want 51 votes within the Senate to substantiate a brand new Fed chair. It’s doable that in 2026, when Jerome Powell’s time period ends, if Trump is president, then a brand new Fed chair could possibly be extra beholden to the White Home. Nonetheless, 5 of the 12 officers on the Federal Open Market Committee won’t have been appointed by the winner of the 2024 election.”

Because you requested (half 1)

Q: What must change for the US inventory market to turn into much less concentrated?

A: Market efficiency on the finish of 2023 may present helpful context for desirous about the long run. Smaller-capitalization shares, as represented by the Russell 2000 Index, superior by greater than 20% within the two months ended Dec. 31, 2023.8 The equal-weight S&P 500 Index outperformed the market-cap weighted S&P 500 Index by greater than 3% throughout the identical interval.9 The outperformance occurred as investor expectations for fee cuts in 2024 elevated from three to 6. It wasn’t to be. US fairness efficiency was more and more extra concentrated within the first half of 2024 as fee minimize expectations had been tempered.

Going ahead, the expectation of an easing cycle and the normalization of the yield curve might assist to once more broaden market participation.

Because you requested (half 2)

Q: Are you involved {that a} US president could take the nation out of North Atlantic Treaty Group (NATO)?

A: No. The Nationwide Protection Authorization Act for Fiscal Yr 2024 prohibits the president from unilaterally withdrawing from NATO with out approval of a two-third Senate super-majority or an act of Congress. As well as, 23 members of NATO (together with France and Germany) are prone to meet NATO’s 2%-of-gross home product army spending dedication this 12 months, up from 11 in 2023 and simply three in 2014.10

Everybody has a podcast

Kristina Hooper, Chief International Market Strategist at Invesco, joined the Higher Potentialities podcast to debate the midyear outlook. Kristina has held quick to her beliefs that the US financial system could be resilient and that the US Federal Reserve would decrease rates of interest this 12 months, maybe greater than as soon as. Her views have had her on the precise facet of markets, and she or he continues to favor publicity to danger belongings within the second half of 2024.

Automate my job?

Every month, I pose a query to ChatGPT – the unreal intelligence-driven chatbot – and assess the response.

Q: Do excessive yield bonds carry out poorly when company bond spreads are tight?

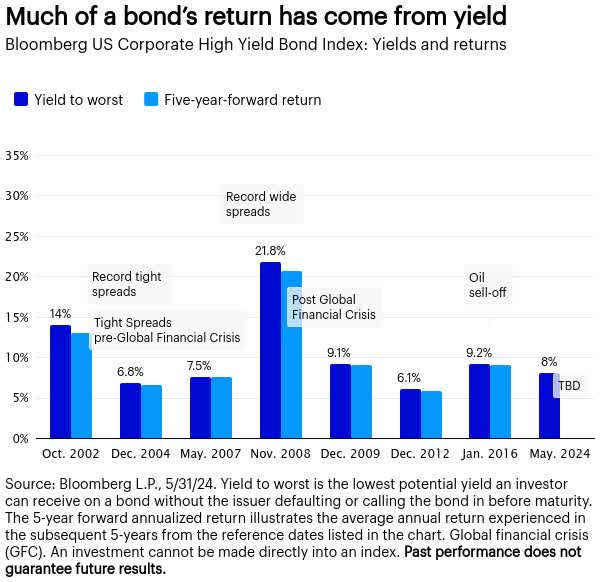

A: Sure, excessive yield bonds are likely to carry out poorly when spreads are tight. It is because tight spreads point out that buyers are demanding much less compensation for the extra danger of holding lower-rated bonds. When spreads are slender, there’s much less room for compensation, and the danger of default turns into extra important relative to the potential return. Consequently, the overall return on excessive yield bonds could also be decrease during times of tight spreads in comparison with durations when spreads are wider, and the risk-return tradeoff is extra favorable.

It is a cheap reply, ChatGPT. I might choose buyers, nevertheless, to treat the yield as an affordable evaluation of the five-year ahead return, regardless of the unfold surroundings. The chart under demonstrates that in many various conditions, a lot of the return comes from the yield. At the moment, the yield of the Bloomberg US Company Excessive Yield Bond Index is 8%.11 That is doubtlessly a worldwide equity-like return, with out the historic volatility of equities.12 I am unsure I might need to eschew an 8% yield just because spreads are tight.

On the highway once more

My travels took me to Minneapolis to satisfy with monetary professionals. I used to be requested in a facet dialog to opine on the brand new petrodollar settlement. Embarrassingly, I used to be stumped by the query. I hadn’t heard something about it, and admitted as such. It turns on the market was good purpose that I missed it. The viral story claimed {that a} 50-year settlement between the US and Saudi Arabia requiring the latter to promote its crude oil exports in US {dollars} had expired. Social media was ablaze with hypothesis that it will end in a deadly blow to the US greenback. I can perceive the priority, however for the truth that the story circulating on social media was pretend. In hindsight, I am comfortable that my minimal social media use left me flummoxed by the query.

Here is how I’d have answered the query had I identified then what I’ve since learn:

- Saudi Arabia and the US by no means had a secret 50-year settlement to promote oil in US {dollars}. It merely benefited each international locations to take action.

- Saudi Arabia has indicated its openness to promote oil in different currencies as properly.

- Saudi Arabia has continued to choose US {dollars}, given its shut financial and army ties to the US coupled with the dominion’s want for {dollars} to move and insure its oil exports.

- Do not imagine every part that you simply learn!

Footnotes

- 1Supply: US Bureau of Financial Evaluation, 5/31/24.

- 2Supply: US Federal Reserve, June 2024.

- 3Supply: Bloomberg, 6/17/24. Based mostly on the distinction between the 10-year US Treasury fee and the 3-month US Treasury fee.

- 4Based mostly on the typical S&P 500 Index efficiency 12 months earlier than and 12 months after the start of the previous 16 easing cycles. Sources: Federal Reserve Financial Database (FRED) and Bloomberg L.P., 5/31/24.

- 5Supply: Bloomberg, 6/17/24. Based mostly on the option-adjusted unfold of the Bloomberg US Company Bond Index.

- 6Supply: US Federal Reserve, 5/31/24. Based mostly on the web % of financial institution senior mortgage officers reporting the tightening or easing of lending requirements to medium and huge companies.

- 7Supply: Fox Enterprise, “Economist Harry Dent predicts inventory market crash worse than 2008 disaster: The ‘bubble of all bubbles,'” 6/10/24

- 8Supply: Bloomberg, 5/31/24.

- 9Supply: Bloomberg, 5/31/24.

- 10Supply: North Atlantic Treaty Group, 5/31/24.

- 11Supply: Bloomberg, 5/31/24. Based mostly on the yield to worst of the Bloomberg US Company Excessive Yield Bond Index.

- 12Supply: Invesco, Bloomberg. Historic volatility measured by the usual deviation of rolling month-to-month 1-year returns for the S&P 500 Index (0.16) and the Bloomberg US Company Excessive Yield Bond Index (0.12) from 7/29/1983 to five/31/2024.

- Above The Noise:Getting Again To Regular by Invesco US