Realty Revenue: High Worth For Revenue Buyers (NYSE:O)

jaturonoofer

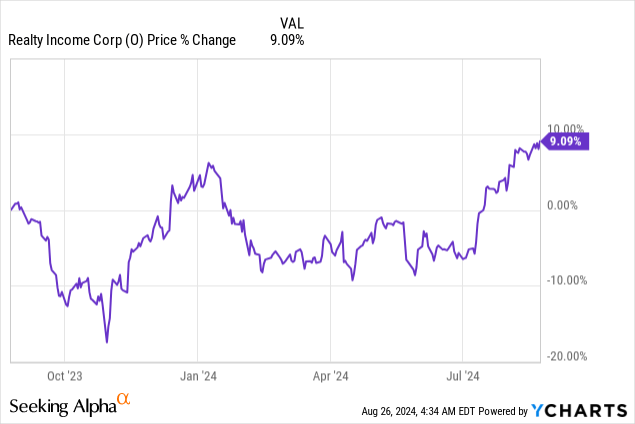

Shares of Realty Revenue (NYSE:O) began to surge in July and have now crossed above $60 for the primary time since July 2024. Realty Revenue delivered sturdy second fiscal quarter earnings at first of the month that confirmed robust AFFO and same-store rental development outcomes, particularly within the industrial portion of the REIT’s enterprise. The Federal Reserve additionally seems to be on the cusp of lastly reducing the federal fund fee, which may lure extra traders in rate-sensitive sectors corresponding to actual property. In my view, Realty Revenue will proceed to develop its dividend, which makes the REIT a prime funding for earnings traders particularly.

Earlier score

I rated shared of Realty Revenue a purchase because of a powerful dividend protection profile, based mostly off of adjusted funds from operations, and sturdy portfolio metrics (lease phrases, diversification, occupancy). In consequence, I figured that the REIT’s shares had been Set For A New Upleg in Might. Realty Revenue’s Q2’24 confirmed continuous promise by way of operational execution, particularly within the industrial phase, and with the Federal Reserve set to strategy its pivot level subsequent month, I imagine that extra investor cash may return to the true property sector and to high-quality REIT decisions like Realty Revenue.

Sturdy AFFO development in Q2, strong dividend protection

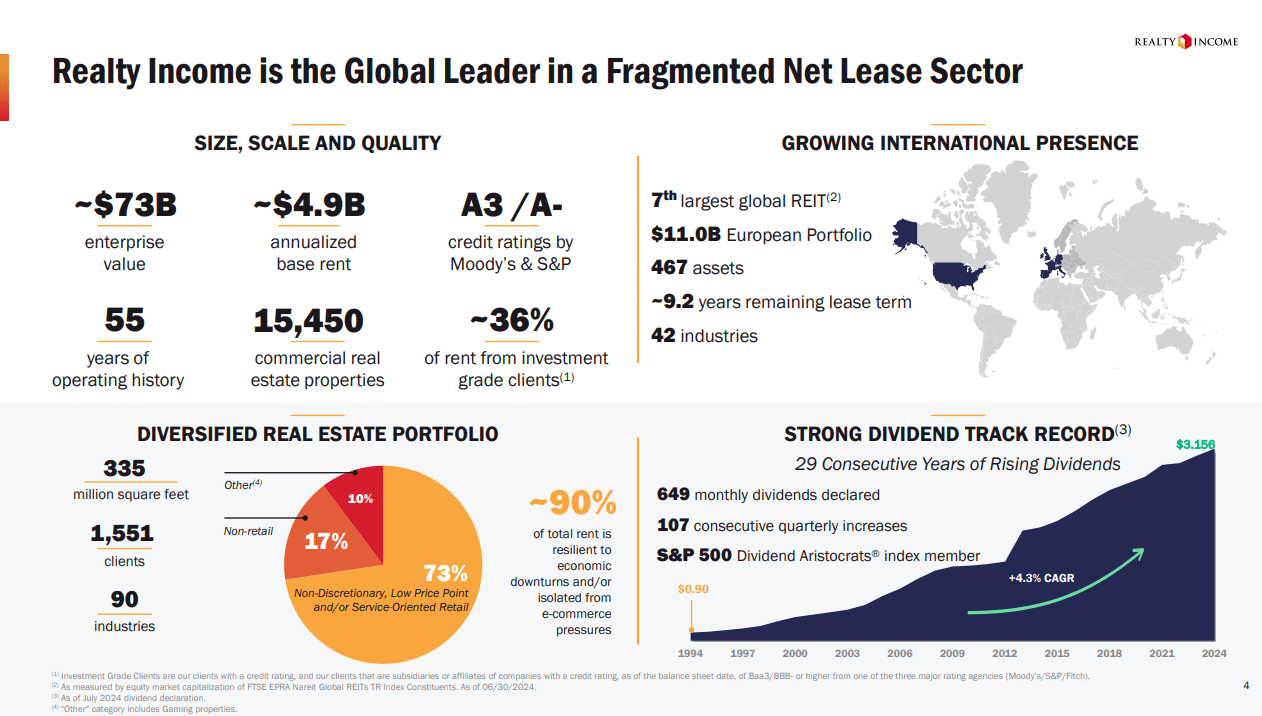

Realty Revenue remained a number one internet lease REIT with a well-performing, diversified portfolio within the second-quarter. The REIT owned a complete of 15,450 industrial actual property properties on the finish of the June quarter, nearly all of which had been situated within the U.S. Most of Realty Revenue’s belongings belong to the non-discretionary sector and subsequently these belongings have a excessive diploma of recurring money circulation.

Realty Revenue

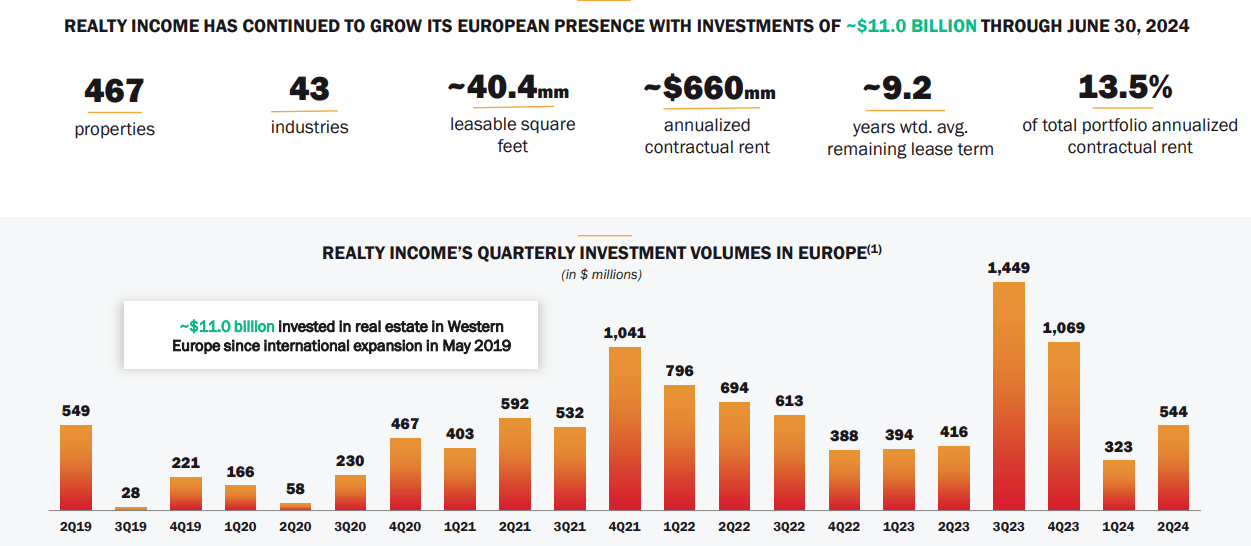

The REIT’s growth in Europe has resulted in Realty Revenue constructing a formidable asset base abroad in recent times as effectively. In Europe, the REIT owned 467 properties valued at roughly $11B on the finish of the second-quarter, and it now has an actual property presence in lots of European nations, together with Germany, France and Portugal. Going ahead, I anticipate Realty Revenue to proceed to put money into lease alternatives (doubtlessly by way of sale-and-leaseback transactions) in core European markets.

Realty Revenue

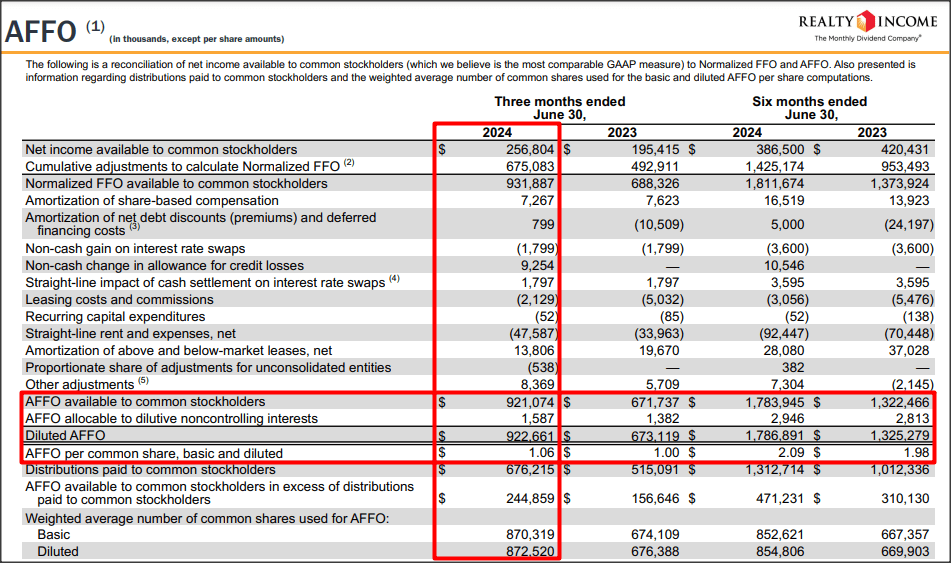

Within the second-quarter, Realty Revenue noticed a lift to its adjusted funds from operations, as previous acquisitions made a constructive affect on the REIT’s most vital metric: adjusted funds from operations.

A REIT’s AFFO is often thought of a benchmark metric and used to calculate dividend protection ratios: within the second-quarter, Realty Revenue generated $922.7M in AFFO (on a diluted foundation) which calculated to 37% year-over-year development. Final yr’s second-quarter outcomes didn’t embrace the properties beforehand belonging to Spirit Realty Capital, a REIT that Realty Revenue acquired final yr with a purpose to enhance its portfolio and AFFO development particularly.

Realty Revenue

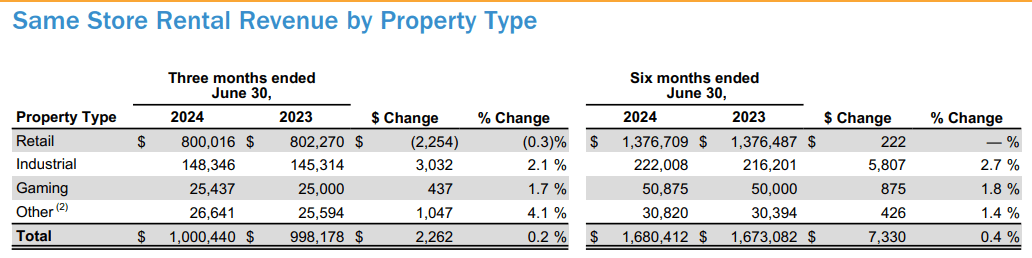

Key to Realty Revenue’s adjusted funds from operations development is that the REIT succeeds in rising its same-store rents… that are depicted within the desk under. Within the first six months of the yr, similar retailer rents elevated 0.4% year-over-year, however they rose particularly rapidly within the industrial phase: industrial properties elevated their same-store lease contributions by 2.7% year-over-year, nearly 6.8X sooner than Realty Revenue’s consolidated outcomes.

Industrial properties represented 14.5% of annualized lease within the second-quarter, which made it the second-biggest funding group after retail. Retail had a income share (on an annualized foundation) of 79.4% on the finish of the June quarter. Going ahead, it might make sense for Realty Revenue to be particularly aggressive by way of rising its publicity to industrial properties.

Realty Revenue

Turning to dividend protection and dividend development.

Realty Revenue’s Q2’24 dividend protection ratio, based mostly off of adjusted funds from operations, was 1.37X in Q2’24 in comparison with 1.31X within the year-earlier interval. The dividend is subsequently very secure and has a excessive sustainability issue, for my part. Realty Revenue can also be persistently elevating its dividend, which makes the REIT a most popular earnings play for dividend traders.

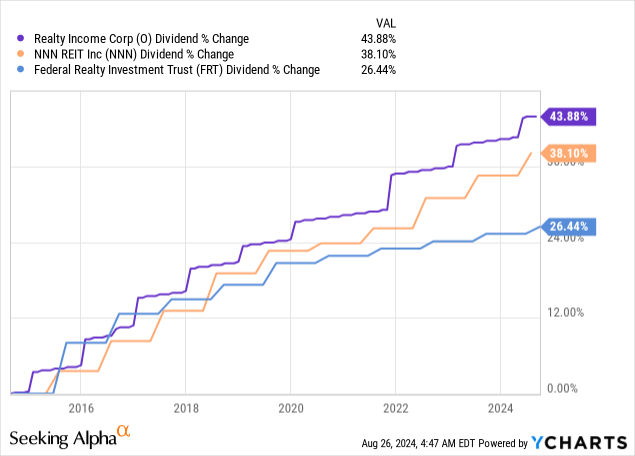

Realty Revenue has beat different internet lease REITs by way of dividend development within the final 10 years and with administration being laser-focused on rising the month-to-month dividend, I imagine it has a great probability of extending this file into the long run. Realty Revenue out-performed different internet lease REITs by way of dividend development, together with NNN REIT (NNN) and Federal Realty Funding (FRT).

Realty Revenue’s valuation

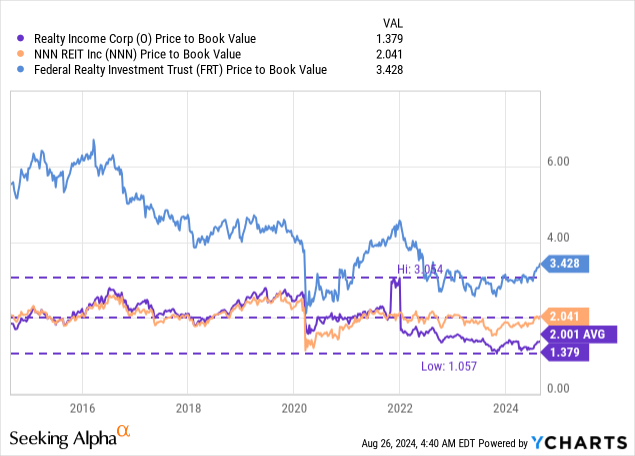

Realty Revenue will be evaluated based mostly off of guide worth because the REIT is a big investor into, principally, U.S.-based actual property. Realty Revenue is at present buying and selling at a price-to-book ratio of 1.38X, which remains to be means under the corporate’s 10-year common price-to-book ratio of two.0X. REITs like Nationwide Retail Properties and Federal Realty Funding commerce at a lot greater P/B ratios, though I do not imagine that is actually justified. Buyers have turned extra bearish on Realty Revenue in latest quarters because of the firm doing quite a lot of acquisitions within the final a number of years.

I anticipate Realty Revenue, given the standard of its dividend/development potential, to return to its historic price-to-book ratio of two.0X in the long run. A revaluation to the longer-term common P/B ratio subsequently implies 45% upside revaluation potential and a good worth within the neighborhood of $88 per-share. This revaluation may very well be pushed by a normalization of rates of interest, which can appeal to extra consumers to the REIT sector.

REITs are additionally typically valued based mostly off of funds from operations, or a spinoff, corresponding to adjusted funds from operations. The distinction between FFO and AFFO tends to narrate to one-off gadgets like transaction or merger bills in addition to non-cash gadgets, and the distinction is often very small on a per-share degree. Realty Revenue and Nationwide Retail Properties have submitted AFFO steerage for FY 2024 (see under) and commerce at P/AFFO ratios of 14.8X and 14.1X. Federal Realty Funding is buying and selling at a P/FFO ratio of 17.1X, based mostly off of funds from operations steerage. The upper multiplier for FRT is probably going because of the firm have an especially lengthy dividend development historical past.

| REIT | Share Worth | FY 2024 FFO Steering | P/FFO Ratio |

| Realty Revenue | $61.77 | $4.15 – $4.21/share | 14.8X |

| Nationwide Retail Properties | $47.02 | $3.31 – $3.37/share | 14.1X |

| Federal Realty Funding | $115.96 | $6.70 – $6.88/share | 17.1X |

(Supply: Writer)

Dangers with Realty Revenue

The most important threat for Realty Revenue, as I see it, is a possible down-turn in industrial actual property. Though the REIT is targeted on long-term leases and has robust occupancy ratios (98.8% in Q2’24), a correction in U.S. actual property would seemingly affect Realty Revenue’s potential to boost rents. Since Realty Revenue is seeing robust development, particularly in its industrial property phase, a slowdown right here would seemingly affect the attractiveness of Realty Revenue as an funding negatively and can also result in weaker dividend protection. Moreover, a slowing growth in Europe is one thing that I might think about to be a detrimental improvement as effectively. What would change my thoughts about Realty Revenue is that if the REIT had been to see a decline in its occupancy charges, weaker same-store development in industrial, in addition to decrease AFFO-based dividend protection ratios.

Remaining ideas

Realty Revenue continues to characterize prime worth at a $61 share worth. Shares have revalued greater within the final two months, which can be associated to traders seeing much less threat in the true property market now that the Federal Reserve is nearing its fee inflection level. Realty Revenue’s monetary outcomes for the second-quarter had been robust, and the REIT confronted no materials challenges to its dividend protection profile. Industrial is doing effectively for Realty Revenue and traders ought to anticipate a rising diversification profile going ahead, with extra investments in industrial in addition to in Europe.