Hoisington Funding Administration Q3 2025 Evaluation And Outlook

David Gyung/iStock by way of Getty Photographs

Idle Crops, AI, and Excessive Tariffs

The mixed results of declining capability utilization in america and globally, the inherently deflationary energy of synthetic intelligence (AI), the Federal Reserve’s deliberate financial restraint, and the liquidity-draining influence of tariffs will serve to impede financial progress and reduce inflation via 2025 and past.

Idle Crops

Opposite to the present typical knowledge, plant capability utilization has declined once more this 12 months within the U.S., the EU, and China. This pattern has persevered because the 2021–22 interval. A weighted index of those economies, plus Japan and the U.Okay., displays this decline (Desk 1). Many factories, refineries, mines, and mills now sit with extra idle capability or function at low utilization charges.

U.S. and International Capability Utilization

|

Peak |

Newest |

% Change |

||

|

1. |

2. |

3. |

||

|

1. |

U.S. |

81.1 |

77.4 |

-4.6% |

|

2. |

Euro Space |

82.9 |

77.8 |

-6.2% |

|

3. |

China |

77.9 |

74.0 |

-5.0% |

|

4. |

International Mixture |

79.1 |

74.8 |

-5.4% |

Supply: Federal Reserve, European Fee, Haver Analytics, Ministry of Economic system, Commerce & Trade, Piper Sandler. International combination consists of Japan and U.Okay.

Desk1

Development of properties, places of work, residences, and different buildings has additionally contracted. The products-producing sector isn’t as massive of a contributor to financial exercise because it was previously, however it nonetheless performs a vital function. As of August 2025, goods-producing employment was lower than 20% the dimensions of personal service-providing employment. Nonetheless, the workweek within the goods-producing sector was 20% longer, and common hourly earnings have been 2.8% increased. This resulted in a far larger contribution to non-public revenue per particular person within the goods-producing sector than within the non-public service sector. Thus, the historic and theoretical work on plant capability utilization as a precursor of financial cycles stays extremely related on this new period.

Capability Utilization

Economists have lengthy tracked capability utilization. Thomas Malthus (1766-1834) was among the many first to jot down about overcapacity and its results, whereas later economists Wesley Clair Mitchell (1874-1948) and Arthur F. Burns (1904- 1987) developed knowledge collection linking capability utilization to enterprise cycles of their influential e book Measuring Enterprise Cycles, (printed in 1946).

Polish-born economist Michał Kalecki (1899–1970) was arguably the primary to position capability utilization on the middle of enterprise cycle principle. Cambridge Economist Joan Robinson (1903–1983) argued that, in free market economies, funding is pushed by anticipated demand. This makes capability utilization—not simply know-how or saving—central to progress dynamics. She expanded this idea into progress fashions, which have been additional developed by others. That is the vital purpose why tax incentives for bodily funding could also be sluggish to have an impact, and why a capital expenditure growth for 2026 is unlikely. That is true even with the favorable new expensing options within the tax code.

Drawing from these and later contributors, economists usually agree that persistently low ranges of capability utilization ought to increase concern in regards to the sustainability of the enterprise cycle for a number of causes:

- Diminished productiveness progress – gear and infrastructure that sit idle contribute nothing to output, slowing the expansion of total effectivity.

- An obstacle to capital formation – companies with idle equipment and buildings don’t develop capability. This depresses new funding spending. Sunk prices of underutilized property play a vital function on this determination.

- Labor market pressures – idle vegetation usually result in layoffs, diminished hours, and weaker demand for native suppliers, amplifying cyclical downturns.

- Revenue compression – extra capability prompts companies to interact in price-cutting to cowl fastened prices, which squeezes earnings.

- Monetary stress – corporations battle to service debt tied to unused property, which raises the chance of bankruptcies and nonperforming loans within the banking system.

- Downward worth pressures – when demand is weak relative to potential provide, companies minimize costs or restrain wage progress, pushing the financial system towards disinflation or deflation.

Combining AI and Tariffs Into the Base Mannequin

AI – Completely different From Prior Improvements

AI must be understood as an evolutionary innovation with a uniquely broad influence: in combination, it is going to scale back—not improve—the elements of manufacturing (the demand for labor, pure assets, and capital). This contrasts sharply with earlier improvements that raised demand throughout these inputs. The outcome aligns with the angle superior in Robert J. Gordon’s The Rise and Fall of American Progress: The U.S. Commonplace of Residing For the reason that Civil Battle (2016).

Gordon discovered that the good American financial progress period of 1870 to 1970 was pushed by 5 innovations: electrical energy, trendy communications, the interior combustion engine, city sanitation, and prescription drugs and chemical substances. These elevated the usage of the elements of manufacturing as a result of they have been revolutionary moderately than evolutionary improvements. In consequence, the AI innovation, being an evolutionary change, will increase financial progress lower than previous improvements.

The enlargement of AI-related industries straight boosts productiveness in digital sectors by shifting demand away from conventional, capital-intensive manufacturing strategies. Already, the outlines of such an consequence have begun to look. From February via August this 12 months, complete industrial manufacturing (IP) remained unchanged, with a small decline within the final two months. IP knowledge doesn’t sufficiently isolate AI manufacturing. Nonetheless, AI sectors seem like offsetting declines all through the opposite industrial sectors. In consequence, the distinct influence of AI has each masked and intensified underutilization in legacy industries, similar to manufacturing and heavy business.

AI is rendering whole sections of the financial system, similar to name facilities and knowledge entry operations, out of date. In distinction to earlier waves of know-how, AI’s broad effectivity enhancements lower demand for bodily constructing supplies and equipment, thereby lowering the multiplier impact on the broader financial system, whilst AI is anticipated to result in enlargement in lots of new sectors. This distinctive type of capital displacement additional depresses utilization charges and new funding in legacy sectors.

AI decreases labor demand by automating cognitive and repetitive duties throughout a variety of service sector expertise. Prior automation primarily affected routine manufacturing unit roles, however AI goes additional. Historically, new graduates gained expertise via duties similar to knowledge assortment and evaluation. Now, AI can do these duties rapidly, sharply lowering the necessity for junior employees. One AI- enabled worker now replaces a number of folks, leading to fewer hiring wants. AI additionally allows companies to automate mid-skill roles, thereby pushing down salaries and shifting decisions from folks to software program. This didn’t occur in prior know-how waves. Stories point out that school graduates already face decrease demand as a result of AI can deal with superior duties. This ends in slower hiring, weaker wage progress, and diminished bargaining energy for employees with out irreplaceable expertise.

This basic change ends in a shift in company revenue relative to family revenue. On the identical time, it creates a disinflationary and even deflationary setting. Automation and protecting insurance policies are reshaping legacy enterprise cycles.

All through historical past, many promising concepts or improvements have drawn substantial investments. Within the early phases, traders usually noticed large positive aspects. Examples embody the monetary bubbles of the 18th century and the dot-com mania of the late twentieth century. As in these instances, returns have been inadequate to justify the huge funds dedicated. Whereas it’s nonetheless unsure if this may occur once more, a repetition of this sample may result in the development of way more plant capability than is required, which might then stay unused and intensify the standard boom-and-bust cycle of those industries.

Tariffs and Retaliation

When a rustic raises tariffs and its buying and selling companions retaliate, a course of is begun which reduces liquidity. After retaliation, a number of inside shocks to liquidity observe. A revenue squeeze instantly impacts these concerned in worldwide commerce as complete revenues fall. Demand falls in micro markets, and costs of products additionally drop since internationally traded items are extremely worth elastic.

Producers reply by chopping demand for labor, pure assets, and capital. This causes a shock to those elements of manufacturing, which then reduces their very own spending. As the present account deficits shrink, worldwide capital flows additionally fall. This ends in a pointy decline in liquidity. Within the Nineteen Twenties and Nineteen Thirties, central banks didn’t offset this loss. The downward pattern persevered till 1939, when World Battle II started.

Financial Restraint

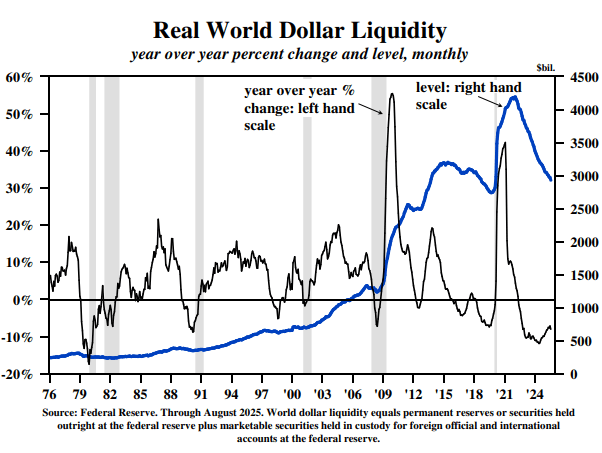

On September 23, Fed Chair Powell acknowledged that the Federal Reserve’s rate of interest stance is “nonetheless modestly restrictive” after the September charge minimize. This restrictive stance has worldwide implications as might be seen in Actual World Greenback Liquidity (RWDL) reaching a post-COVID low in August (thick blue line, Chart 1). All the RWDL will increase ensuing from the pandemic have been reversed. Up to now 12 months, RWDL decreased by 8% (skinny line, Chart 1), in comparison with a median annual improve of 5.8% since 1976. On this extra restrictive setting, the Fed’s coverage accelerates overcapacity in legacy industries that also make up a good portion of family revenue and jobs. Heavy funding flows into AI has shifted monetary assets away from legacy industries. Over the past twelve months, industrial financial institution lending remained unchanged, after excluding loans to non-depository monetary establishments, essentially the most extremely leveraged entities on the steadiness sheet. The skew in financial institution lending, rising bankruptcies to multi-year highs, falling credit score scores, and rising delinquencies all recommend that family and small enterprise liquidity is turning into more and more scarce.

Chart 1

Gross Output

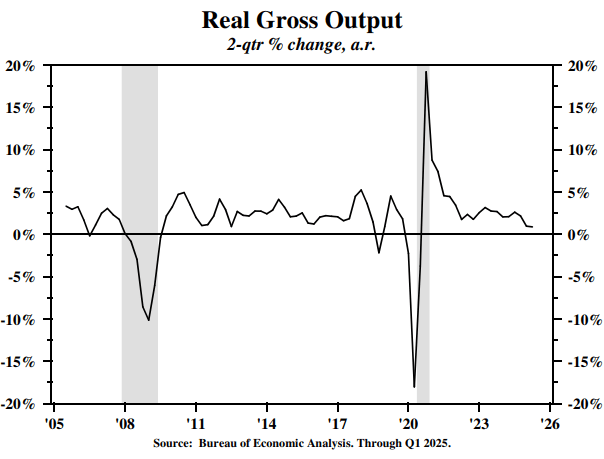

This 12 months, the month-to-month scenario report of the BLS has deteriorated to such an extent that just about all the modest improve in payroll jobs is within the low-paying well being and social companies class. On the identical time, actual GDP has remained resolutely robust.

The problem is easy methods to resolve this discrepancy. The reply is supplied by a statistic referred to as Gross Output (GO) – a measure of spending in any respect phases of manufacturing. Developed by economist Mark Skousen, the Bureau of Financial Evaluation now publishes GO within the last revision of the quarterly Nationwide Earnings and Product Accounts. Within the first quarter, actual GO was $40.9 trillion, 72% greater than actual GDP. In stark distinction to actual GDP, the two-quarter transferring common progress in actual GO decelerated steadily and considerably after 2022, dropping to a paltry lower than 1% annual charge of progress within the first half of this 12 months (Chart 2). Thus, GO and the job statistics are strongly aligned with the well-established mannequin of falling plant capability utilization and the probably influence of AI and tariffs. Actual GO is extra affirmation that financial situations are weaker than usually believed.

Chart 2

Concluding Ideas

Brief-term coverage charges have declined within the U.S., the EU, and different essential nations. Extra charge reductions are additionally usually anticipated within the monetary markets. These actions, nevertheless, are prone to be inadequate so long as RWDL continues to contract. Thus, the Fed coverage is a persistent headwind for financial progress. We stay dedicated to a long-duration technique for U.S. Treasury bonds, regardless of many traders remaining extraordinarily pessimistic in regards to the outlook for these securities.

Van R. Hoisington | Lacy H. Hunt, Ph.D.

|

DISCLOSURES Hoisington Funding Administration Firm (HIMCo) is a federally registered funding adviser positioned in Austin, Texas, and isn’t affiliated with any father or mother firm. The knowledge on this market commentary is meant for monetary professionals, institutional traders, and consultants solely. Retail traders or most of the people ought to communicate with their monetary consultant. Data introduced is for instructional functions solely and doesn’t represent a suggestion or solicitation for the sale or buy of any securities, funding merchandise or advisory companies. Data herein has been obtained from sources believed to be dependable, however HIMCo doesn’t warrant its completeness or accuracy; opinions and estimates represent our judgment as of this date and are topic to vary with out discover. This memorandum expresses the views of the authors as of the date indicated and such views are topic to vary with out discover. HIMCo has no responsibility or obligation to replace the data contained herein. This materials is meant as market commentary solely and shouldn’t be used for some other functions, together with making funding selections. Sure data contained herein regarding financial knowledge relies on or derived from data supplied by impartial third-party sources. Charts and graphs supplied herein are for illustrative functions solely. This memorandum, together with the data contained herein, might not be copied, reproduced, republished, or posted in entire or partially, in any kind with out the prior written consent of HIMCo. |

Editor’s Be aware: The abstract bullets for this text have been chosen by In search of Alpha editors.