CarGurus: The Rebound Rally Has Steam (NASDAQ:CARG)

Aleksandr Potashev/iStock Editorial by way of Getty Photos

Generally, turnaround tales require a little bit of persistence: however they make for nice holds whereas the remainder of the inventory market is exceedingly costly. And with record-breaking S&P 500 multiples, I am positioning increasingly more of my portfolio into these value-oriented rebound performs.

CarGurus (NASDAQ:CARG) is a inventory that I am notably keen on. The net automobile market has shed its car-flipping enterprise and refocused again on its vendor promoting community. Having restored its market enterprise again to progress, the inventory is now up ~7% 12 months thus far, lagging behind the S&P 500 however carrying loads of ahead potential.

With progress in paid vendor counts, the bull case appears to be like brilliant, and at affordable multiples

I final wrote a bullish opinion on CarGurus in April, when the inventory was nonetheless buying and selling within the ~$22 vary. Since then, the corporate has launched super Q1 outcomes that confirmed two essential issues: acceleration in market income progress, and a return to progress within the variety of paid sellers within the firm’s community once more. With CarGurus solidly positioned for growth in its market platform, I am reiterating my purchase score on this inventory – particularly as the remainder of the market has climbed as much as nosebleed ranges.

As a refresher for buyers who’re newer to this inventory, right here is my up to date long-term bull case for CarGurus:

- CarGurus has made itself important for automobile dealerships. Even earlier than including CarOffer and Prompt Max Money Provide, CarGurus was lengthy thought-about by dealerships to be a essential accomplice as a result of quantity of internet visitors flowing by means of its web site nationwide. By including the power for dealerships to purchase automobiles by means of the CarGurus community as nicely, CarGurus has successfully simply doubled its pockets share throughout the used-car trade.

- Dependable recurring income streams which have a confirmed historical past of working by means of down cycles. CarGurus enjoys a gentle stream of price revenue from its paying automobile dealerships. Quarterly common income per automobile dealership additionally continues to rise. CarGurus has additionally confirmed itself able to managing by means of downturns, swiftly performing to assist struggling dealership clients within the fast aftermath of COVID however now recovering even after these actions.

- CarGurus stays the #1 web site for used-car analysis within the U.S., and by a large margin. By default, automobile dealerships (or any enterprise, actually) will go the place the eyeballs are, and CarGurus has cemented its place because the main web site to do analysis earlier than shopping for a used automobile.

- Visitors growth- Month-to-month lively customers and internet periods proceed to rise, showcasing CarGurus’ reputation with customers.

- Enhancing wholesale results- CarGurus has now totally built-in CarOffer into its enterprise and stabilized its profitability, giving the corporate an enormous edge within the dealer-to-dealer community and increasing its attain.

Despite all of those strengths, and in addition despite the inventory’s latest rally, CarGurus nonetheless trades at fairly low-cost multiples. At present share costs close to $25, CarGurus trades at a market cap of $2.63 billion. After we internet off the $246.3 million of money on CarGurus’ most up-to-date stability sheet, the corporate’s ensuing enterprise worth is $2.38 billion.

For subsequent fiscal 12 months (FY25), Wall Avenue analysts have a consensus income estimate of $967.1 million for the corporate, representing 10% y/y progress (after a -4% anticipated decline this 12 months, primarily pushed by more durable comps from the intentional shrinkage of the wholesale enterprise). If we conservatively assume a 23% adjusted EBITDA margin on that income (in keeping with Q1 outcomes, which confirmed ~6 factors of y/y adjusted EBITDA margin growth), adjusted EBITDA subsequent 12 months can be ~$222 million.

This places CarGurus’ valuation multiples at:

- 2.5x EV/FY25 consensus income

- 10.7x EV/FY25 estimated adjusted EBITDA

To me, these multiples are fairly a cut price for a corporation that has returned its focus to a high-margin, recurring-revenue web promoting enterprise. Keep lengthy right here and hold using the latest rebound increased.

Q1 obtain

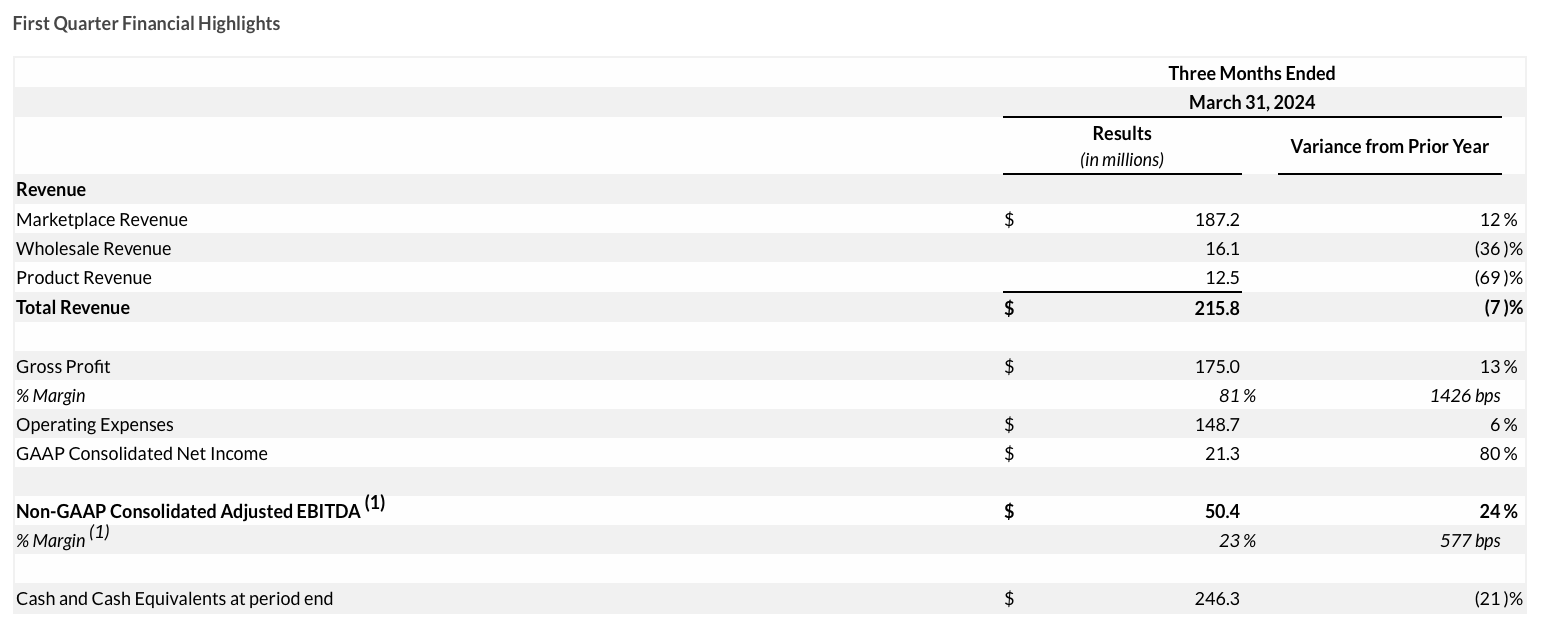

Let’s now undergo CarGurus’ newest quarterly ends in higher element. The Q1 earnings abstract is proven beneath:

CarGurus Q1 outcomes (CarGurus Q1 earnings deck)

Whole income declined -7% y/y to $215.8 million, which as beforehand talked about is pushed primarily by deliberate declines in product and wholesale income. Nevertheless, market income progress of 12% y/y accelerated versus 10% y/y progress in This fall.

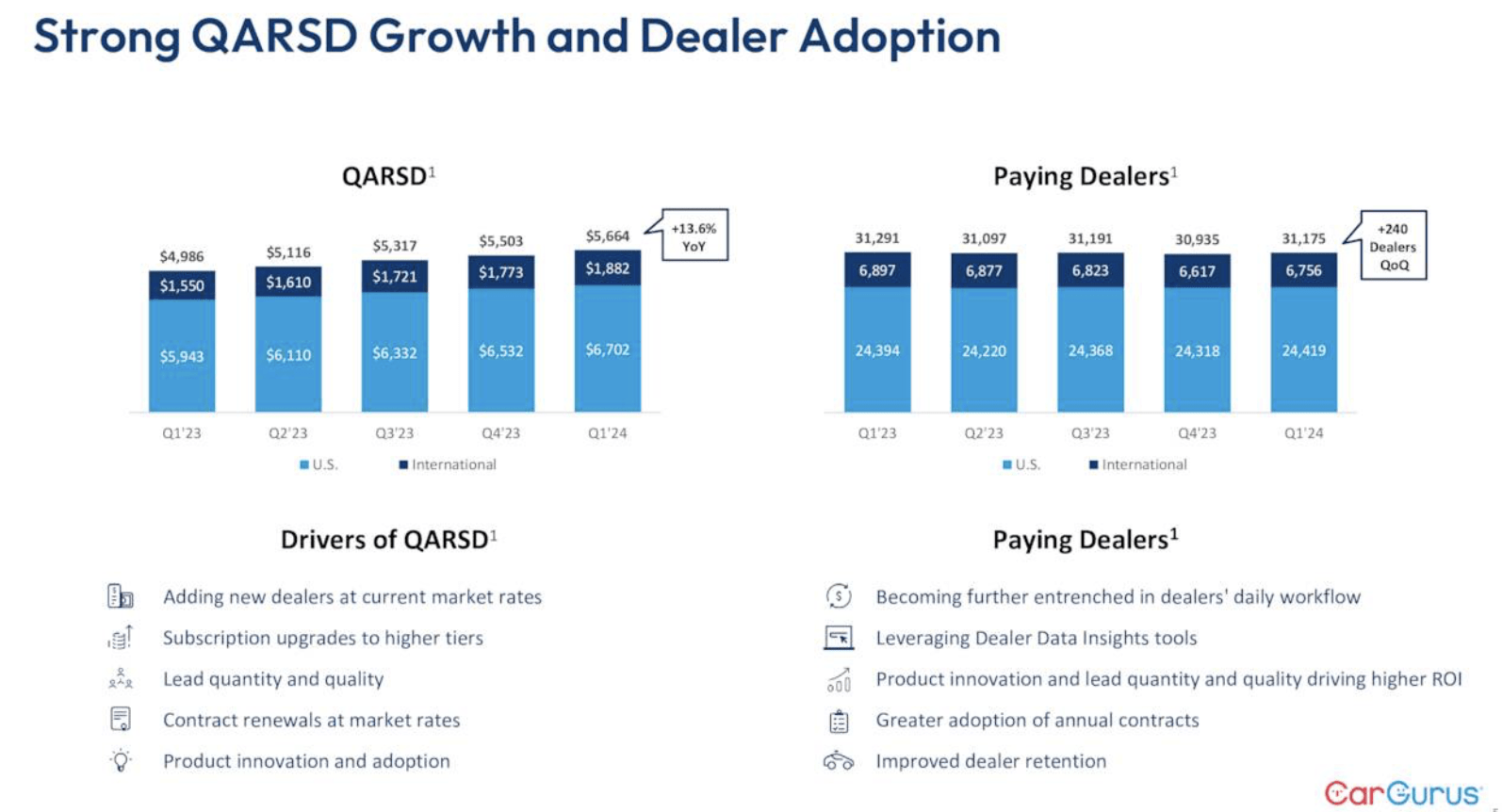

Maybe much more encouraging to see within the quarter: CarGurus’ rely of paid sellers returned to sequential progress, including 240 net-new sellers within the quarter to finish at 31.2k complete within the buyer base, reversing a number of quarters of sequential decline. Not solely that, however common quarterly income per dealership additionally elevated 14% y/y to $5,664, which the corporate chalked as much as signing up new sellers and renewing present sellers at increased prevailing market charges.

CarGurus vendor metrics (CarGurus Q1 earnings deck)

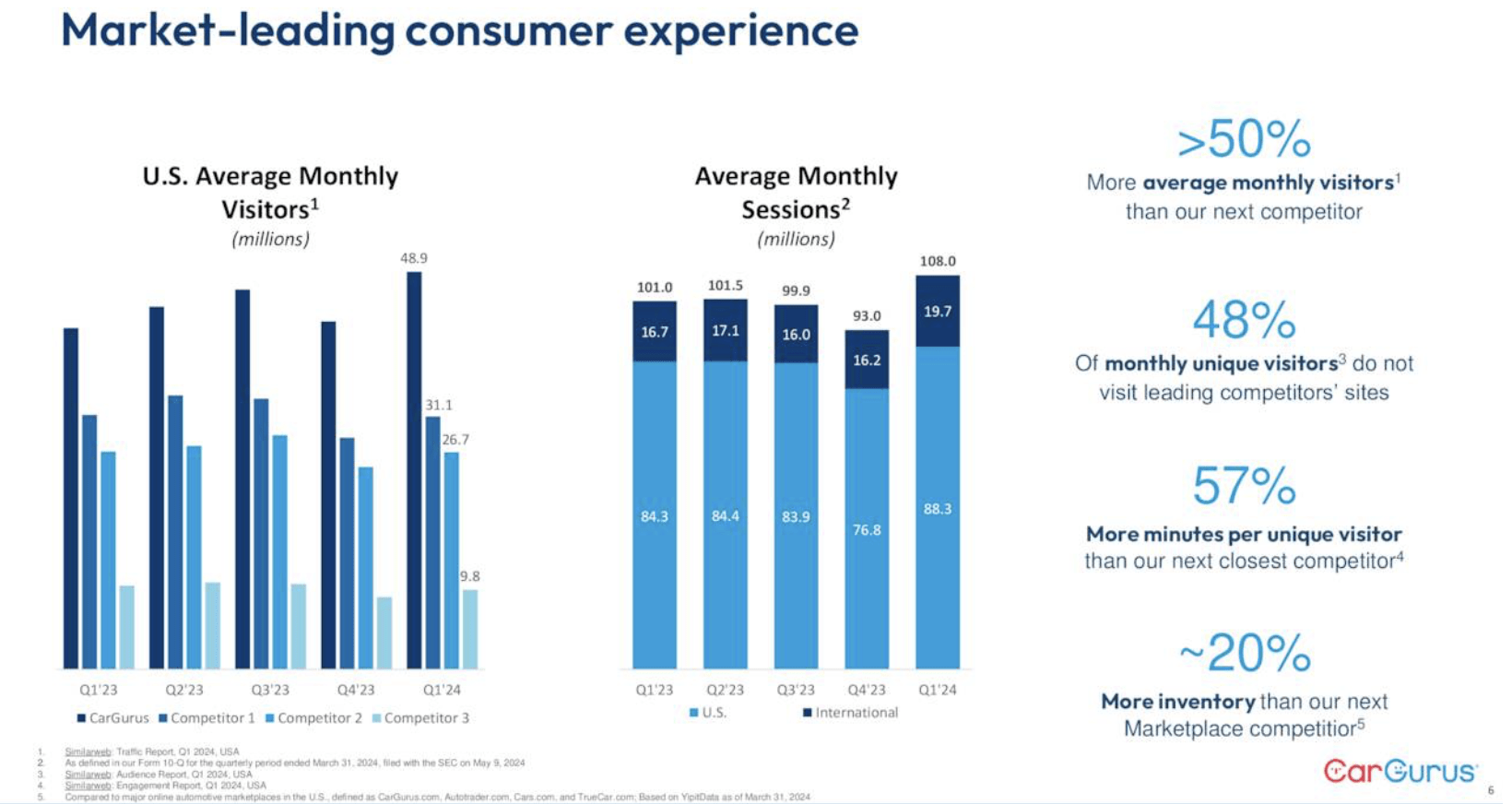

But it surely’s not simply on the vendor facet that CarGurus is profitable: the corporate can be rising its footprint with customers as nicely. Common month-to-month periods within the quarter grew 7% y/y to 108 million, and common month-to-month web site guests additionally grew:

CarGurus visitors knowledge (CarGurus Q1 earnings deck)

Talking to the elements which are driving shopper visitors on the Q1 earnings name, CEO Jason Trevisan famous as follows:

Our app continued to be the primary automotive app by way of downloads throughout iOS and Android and one among our fastest-growing channels. Our app generated greater than 1 / 4 of complete leads and app customers averaged greater than three periods per week with robust engagement and loyalty. Roughly 70% of app customers in the end registered with us, permitting us to supply more and more personalized consumer experiences with suggestions tailor-made to their preferences and desires.

We proceed to supply our customers the most important collection of used and new automobiles. Within the first quarter, we grew our out there listings by 30% year-over-year, and we ended the quarter with roughly 20% extra out there stock than our subsequent closest automotive competitor. We ended the quarter as essentially the most visited automotive market with 57% extra complete visits than our subsequent closest competitor, and 48% of our month-to-month distinctive guests didn’t go to our main opponents’ web sites. Our internet promoter rating remained extraordinarily excessive with 90% of consumers stating that they might advocate CarGurus to a good friend.”

Profitability additionally soared within the quarter, with adjusted EBITDA progress of 24% y/y to $50.4 million outpacing income progress, and adjusted EBITDA margins rising six factors y/y to 24%.

Key takeaways

Shunned for years by a slower vendor market within the fast aftermath of the pandemic, CarGurus is now roaring again with a transparent deal with increasing its market enterprise, which is gaining each new dealerships in addition to substantial new shopper visitors ranges. With the inventory persevering with to commerce at discounted multiples, proceed holding on right here for extra upside.