The TJX Firms Inventory: Actuality Verify On The Treasure Hunt Offers (NYSE:TJX)

pixelfit/E+ through Getty Photos

Funding Thesis

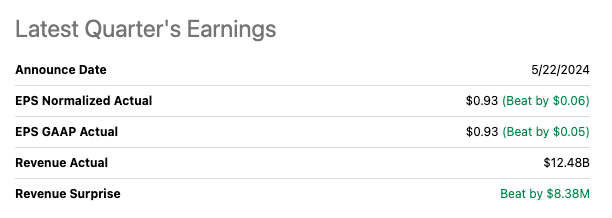

TJX Firms (NYSE:TJX), the father or mother firm of low cost retailers like TJ Maxx, Marshalls, and HomeGoods, reported a stellar first quarter for fiscal 2025. Each gross sales and earnings surpassed expectations, sending the corporate’s inventory value hovering.

Gross sales grew by 6% YoY to $12.5 billion, exceeding estimates. This optimistic efficiency was pushed completely by a rise in buyer visitors, with comparable retailer gross sales rising by 3%. Earnings per share additionally impressed, leaping 22.4% to $0.93 per share, exceeding expectations of $0.87.

SeekingAlpha

I imagine the corporate’s sturdy efficiency may be attributed to a number of elements. Inflation is pushing shoppers in direction of value-oriented retailers, making TJX’s choices extra engaging. Moreover, TJX has strengthened its relationships with manufacturers, resulting in a greater diversity of high quality merchandise at decrease costs. They’ve additionally cultivated a buying expertise that’s seen as enjoyable and classy, attracting youthful demographics with their “treasure hunt” method as Ernie Herrman, the corporate CEO, described over the past earnings name:

I believe what provides us a number of confidence is we’re the one retailer proper now that I see that is ready to take manufacturers and trend and high quality and put all of that collectively on this treasure hunt format, bear in mind, I am speaking about having good, higher, finest good, higher, finest, our vary of all revenue and age teams, whereas all the opposite retailers, and I do know, Matt, we have talked about this earlier than, I actually do not know of some other retailer brick-and-mortar oriented that’s making a treasure hunt of this pleasure degree and leisure degree as a result of they’re buying and selling so broadly as we’re.

Wanting forward, TJX expects continued progress in comparable gross sales and market share. The corporate is optimistic about its potential to ship sturdy monetary efficiency within the incomes quarters of fiscal 2025.

On this article, I goal to seek out if TJX is a strong candidate for my worth with potential portfolio. To perform this, I’ll discover numerous elements like Administration effectiveness, company technique, and valuation metrics to find out if its aligned with this funding model.

Administration Analysis

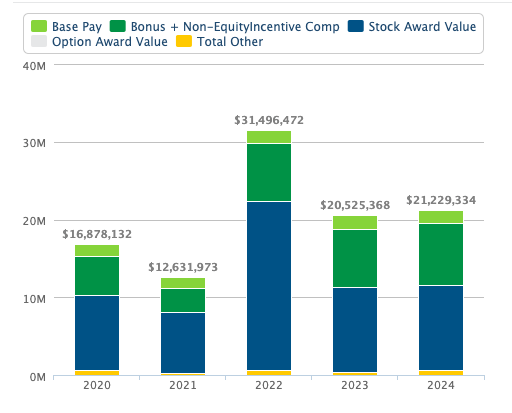

Ernie Herrman, CEO of TJX Firms since January 2016, has a surprisingly excessive approval score on Glassdoor contemplating the character of the enterprise. This is perhaps because of his lengthy tenure with the corporate, the place he began in 1989. Nevertheless, his excessive inventory award compensation raises some issues.

Wage.com

Throughout the final earnings name, Herrman highlighted the next key factors:

- Development Plans: TJX is concentrated on sustaining its worth proposition by way of a stability of selective value will increase and strategic shopping for to make sure they continue to be aggressive.

- Buyer Acquisition: The corporate is efficiently attracting youthful demographics whereas sustaining a wholesome stability throughout age and revenue teams. That is doubtless because of their “treasure hunt” buying expertise and emphasis on good, higher, finest model assortments.

- Market share: Herrman sound assured within the firm’s potential to achieve market share because of its versatile enterprise mannequin, notably in HomeGoods, the place they will alter classes primarily based on demand.

- Competitors: Whereas Herrman point out that competitors does exist, he believes their sturdy vendor relationships and concentrate on worth give them an edge.

- Worldwide growth: the corporate appears to at all times be in search of growth alternatives however stays tight-lipped about specifics till bulletins are prepared.

Glassdoor

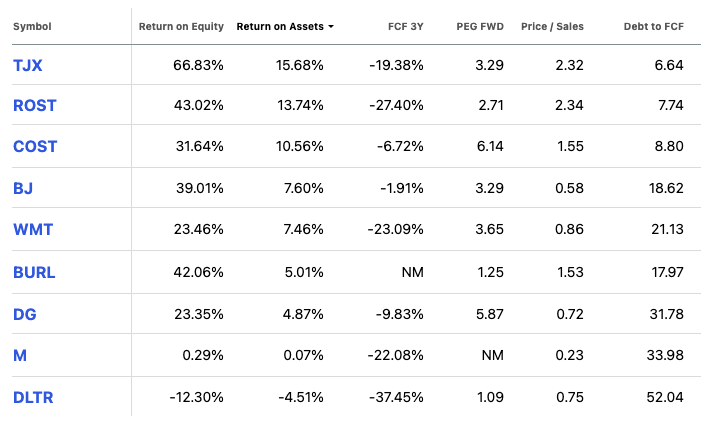

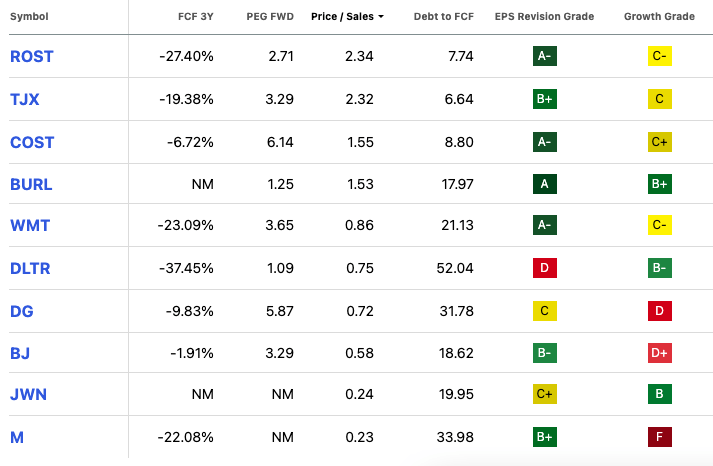

John Klinger, the CFO of TJX, has a protracted historical past with the corporate and has overseen a interval of sturdy monetary efficiency. Regardless of some current smooth income steerage which I imagine is because of momentary financial elements, TJX stays worthwhile with a excessive ROA of 15%- vs a sector median of 4.20% and an ROE of 66%- vs sector median of round 12%. Their leverage ranges are additionally low at a Debt to FCF of 6x, one of many lowest when in comparison with different opponents within the business as highlighted beneath. Throughout the earnings name Klinger identified to the next:

- Buyer Development: throughout totally different revenue ranges

- Profitability: by way of expense administration and stock administration

- Growth plans: worldwide section is predicted to succeed in its progress goal at 8% and core enterprise inside Marmaxx stays sturdy regardless of climate challenges.

- Buyer Expertise: concentrate on remodels and shrink administration. Additionally talked about that regardless of not having a big penetration with their bank card like some opponents, they use numerous information sources apart from bank cards to know demographics and traits.

General, I discover that TJX workforce seems well-positioned to keep up their management within the off-price retail sector. Their concentrate on a compelling worth proposition, buyer acquisition throughout demographics, strategic growth, however notably I discover that their dedication to the brick and mortar buying expertise positions them for continued success on this area of interest sector the place bodily retailer gross sales are nonetheless taking place.

Nevertheless, I do imagine, that their potential to efficiently keep this pattern and stability it with the rising significance of on-line retail and potential brief time period financial headwinds might be essential elements within the coming years.

Lastly, I’ve confidence within the administration because of the mixture of tenure with the corporate and expertise within the business and because of their success within the final years I’m inclined to provide administration a “Exceeds Expectations”.

SeekingAlpha

Company Technique

TJX Firms, recognized for TJ Maxx, Marshalls, and HomeGoods, focuses on world growth because the main off-price retailer. I discover that their technique revolves round:

- Geographic Development: US, Canada, and Europe (with emphasis in Germany and the Netherlands)

- Treasure Hunt expertise: providing a always altering number of model title attire and homeware at vital reductions

- Transaction Development: prioritize buyer transactions reasonably than relying solely on greater spending per go to.

- Give attention to worth: sturdy worth proposition for broad buyer base

TJX Web site

Here’s a desk I created with key differentiators between TJX and a few corporations within the business providing comparable providers:

|

TJX Firms |

Ross Shops (ROST) |

Burlington (BURL) |

|

|

Off-Worth Retailer Market Share |

68% |

22% |

10% |

|

Company Development Technique |

Worldwide growth (US, Canada, Europe). Give attention to transaction progress. |

Geographic growth (US) caters to value-conscious shoppers. |

Geographic growth (US), concentrate on household buying expertise |

|

Benefits |

Robust model recognition, various product combine (attire, house items) greater common buyer spend. |

Robust buyer loyalty, concentrate on worth proposition. |

Wider number of household attire and residential items, concentrate on promotional pricing. |

|

Disadvantages |

Decrease on-line presence in comparison with opponents. |

Much less emphasis on house items in comparison with TJX. |

Decrease model recognition in comparison with TJX and Ross. |

Supply: From corporations’ web site, displays, SeekingAlpha, Bloomberg

Whereas TJX dominates the off-price market, opponents like Nordstrom Rack (JWN) and Saks Off 5th (non-public), that are a pending merger talks, supply distinct experiences by concentrating on totally different audiences who’re extra style aware with a concentrate on clearance merchandise and extra choose product combine at a slight greater value. Additional Ross Shops has much less concentrate on house items and Burlington a concentrate on household buying. One other vital distinction is that in contrast to its opponents, TJX has chosen to prioritize brick and mortar. Their on-line presence stays restricted; nonetheless, their on-line choice shouldn’t be as intensive. I imagine this technique is geared toward encouraging frequent visits to shops. Nevertheless, it is a double edge sword, as it would put them at a drawback as on-line buying continues to develop and youthful generations change into a bigger a part of their buyer base.

In the mean time, nonetheless, I imagine their technique is working as their revenue margin stay excessive to different opponents and have low leverage which suggests they’ve the monetary assets to spend on new buying applied sciences.

Wanting forward, whereas TJX present technique positions them effectively, my view is that their long run success hinges on adaptation. Their concentrate on geographic progress, “treasure hunt”, and worth proposition creates a powerful basis. Nevertheless, embracing on-line buying by way of a extra sturdy platform is crucial to succeed in youthful generations and improve their market share. Moreover, capitalizing on sustainability by integrating accountable sourcing practices can appeal to environmental acutely aware prospects. By repeatedly adapting to the evolving retail panorama, TJX can solidify their management in off-price retail and develop their attain.

Valuation

TJX at present trades at round $112.21 The inventory is up round 12% since its final reported earnings in mid-Could and its hitting All-time highs. The inventory can be up round 20% TR YTD.

Now, to evaluate its worth, I employed a 11% low cost price, this price displays the minimal return an investor expects to obtain for his or her investments. Right here, I’m utilizing a 5% threat free price, mixed with the extra market threat premium for holding shares versus threat free investments, I’m utilizing 6% for this threat premium. Whereas this could possibly be additional refined, decrease or greater, I’m utilizing it as a place to begin solely to get a gauge utilizing unbiased market expectations.

Then, utilizing a easy 10 12 months two staged DCF mannequin, I reversed the formulation to resolve for the high-growth price, that’s the progress within the first stage.

To realize this, I assumed a terminal progress price of 4% within the second stage. Predicting progress past a 10-year horizon is difficult, however in my expertise, a 4% price displays a extra sustainable long-term trajectory for mature corporations that must be near historic GDP progress. Once more, these assumptions may be greater or decrease, however from my expertise I’ll use a 4% price as a base case situation because of the nature of their enterprise. The formulation used is:

$112.21 = (sum^10 EPS (1 + “X”) / 1+r)) + TV (sum^10 EPS (1+g) / (1+r))

Fixing for x = 18%

This counsel that the market at present costs TJX EPS to develop at 18%. Based on Looking for Alpha analyst consensus EPS over the subsequent 3-5 years CAGR at 8.21%. Due to this fact, it appears that evidently TJX is overvalued on a elementary foundation and the market is perhaps anticipating that it’s going to develop quicker. Nevertheless, this expectation of 18% progress is perhaps unrealistic, that’s the inventory is overvalued by double the expansion price in EPS with a good worth of $63.55 on DCF foundation.

Additional, I’ll additionally take a look at their ahead value earnings to progress (PEG) ratio which sits at 3.29x -versus a sector median of 1.45x- implying the inventory value is above the business. As well as, their ahead value to gross sales (P/S) ratio appears overvalued at 2.25x -vs 0.89x. Nevertheless, when in comparison with a choose group of corporations, highlighted beneath, which might be thought of leaders within the business, these combined alerts make extra sense, and the corporate appears considerably overvalued:

SeekingAlpha

Regardless of this overvaluation in keeping with elementary metrics like DCF and ratios, I imagine this overvaluation is justified as TJX is extra worthwhile and fewer levered than its fundamental opponents. The upper profitability, progress prospects, and powerful management makes the case for this greater valuation.

Nevertheless, I do imagine that as the corporate is hitting all-time highs to be extra “optimistic cautious” as many expectations are already constructed into the present valuation. Due to this fact, endurance is perhaps rewarded by ready for a weak point. Due to this fact, I’m inclined to begin my protection of TJX with a “Cautious Purchase”.

Technical Evaluation

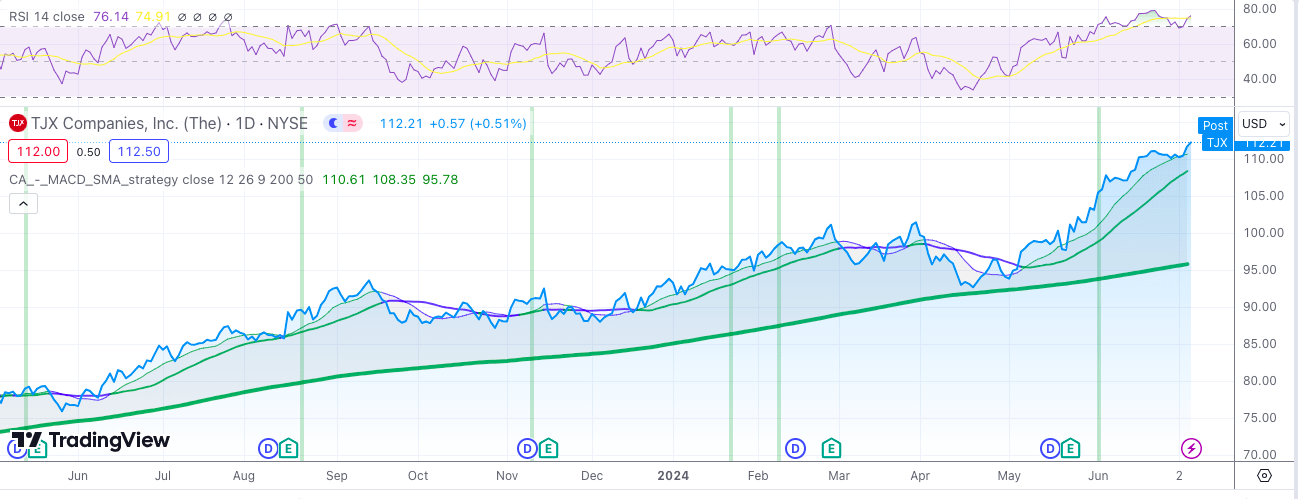

TJX has been on a optimistic momentum since they final reported earnings in mid-Could. The inventory has been hitting all-time highs ever since. Nevertheless, the inventory appears overvalued by now, on a technical foundation, with its 1-year common RSI in overbought territory at 76 and beneath its 14-day shifting common of 74 indicating the inventory value is perhaps altering traits.

TradingView

TJX has shaped a powerful help degree at round $100 and the resistance degree is tough to inform because the inventory is breaking all time highs since its final earnings report and a value correction is feasible. That is why I am beginning my protection of TJX with a “cautious purchase” and can think about a very good alternative close to the $100 mark. Subsequent earnings report is August twenty first.

Takeaway

TJX Firms, impressed with a stellar first quarter. Robust financials, a concentrate on worth, and a loyal buyer base make them engaging. Nevertheless, the inventory’s all time excessive and comparable valuation metrics raises issues about overvaluation. Expertise management and a worldwide growth technique bode effectively for the long run. Their “treasure hunt” buying expertise is a power, however a restricted on-line presence in comparison with opponents is a weak point. Contemplating the potential overvaluation, I’m inclined to begin protection with a Cautious Purchase method as I might be a purchaser on a weak point.