Seagate Know-how Inventory: AI Information Demand Can Push Shares To An All-Time Excessive (NASDAQ:STX)

JHVEPhoto

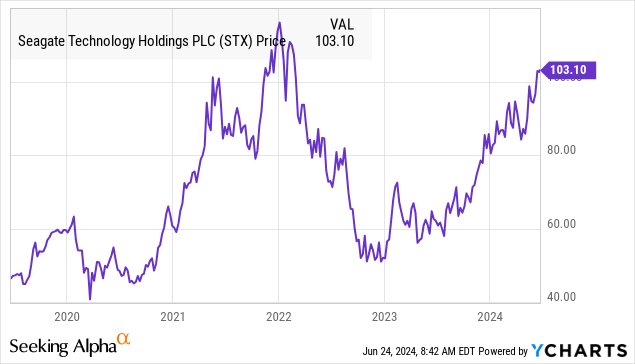

Shares of Seagate Know-how Holdings plc (NASDAQ:STX) have gained momentum because the firm’s newest quarterly outcomes. The inventory is up practically 70% over the previous yr, benefiting from a rebound in earnings.

Whereas the mass-capacity information storage market has confronted uncertainties lately, new demand from cloud computing purposes the place the expertise continues to be thought of probably the most cost-effective choice helps a optimistic outlook.

We final coated STX practically three years in the past highlighting the corporate’s efforts to stay related regardless of the rise of solid-state drives (“SSD”). For anybody conserving observe, the inventory is up from that final article publication date.

In some ways, Seagate’s outlook has advanced even higher than we anticipated and we are able to reaffirm a bullish view on the inventory. Notably, the emergence of synthetic intelligence as a significant market theme and its data-intensive infrastructure represents a brand new development driver we consider can take the inventory to a brand new all-time excessive.

STX Financials Recap

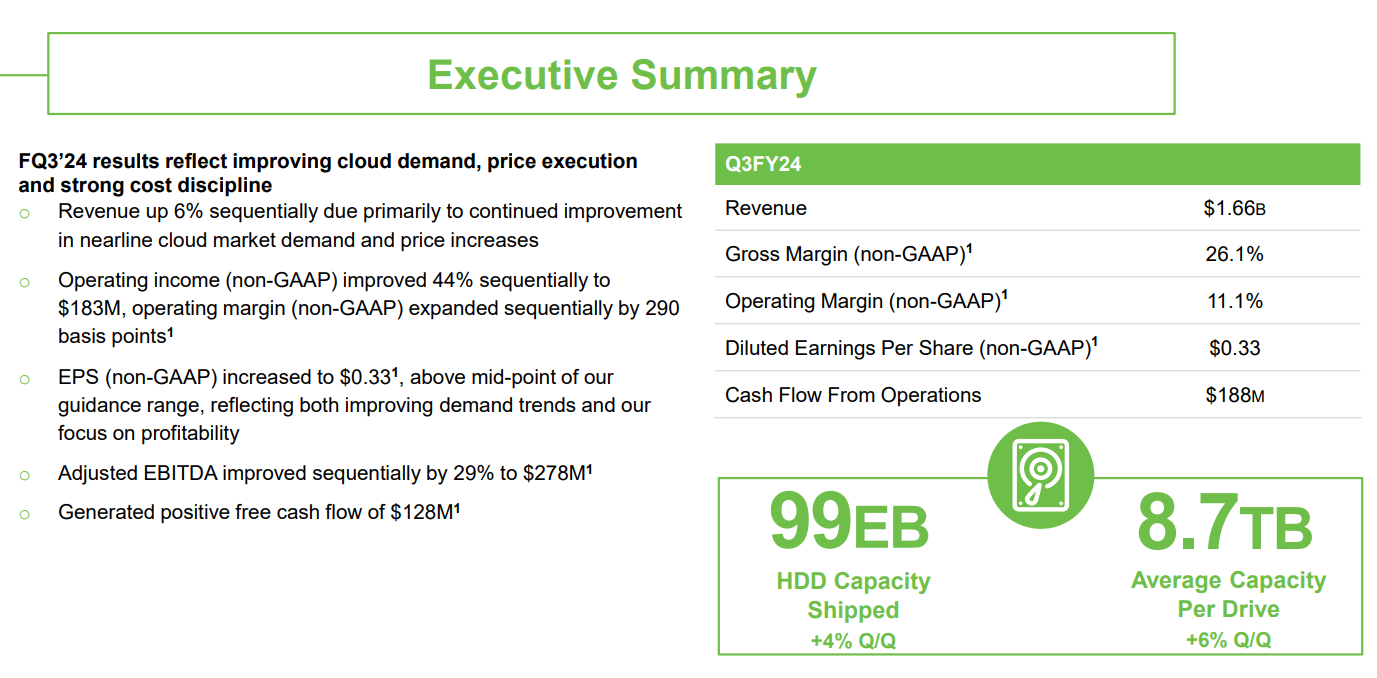

Seagate reported its Q3 fiscal 2024 earnings again in April, with the headline EPS of $0.33 coming in $0.07 forward of consensus, and reversing the lack of -$0.28 within the prior-year quarter. Income of $1.7 billion was down by 11% year-over-year, but in addition forward of estimates.

The story for the corporate has been the continued secular decline of hard-disk-drive (“HDD”) in sure purposes which have shifted towards SSDs. Nonetheless, the developments counsel a stabilization with whole income up sequentially from Q3.

Extra importantly, efforts by Seagate to extend pricing, management prices, and rationalize the enterprise are being mirrored within the climbing profitability.

The non-GAAP gross margin this quarter reached 26.1% in comparison with 18.7% in Q3 2023. The adjusted working margin has additionally surged larger to 11.1% from simply 3.5% within the interval final yr. Q3 adjusted EBITDA of $278 million was up 29% sequentially from $216 million in Q2.

supply: firm IR

The AI Alternative for STX

The message from administration is that buyer and end-market demand are bettering and anticipated to even speed up going ahead. When it comes to steering, Seagate expects This fall income between $1.85 billion representing a 16% enhance from This fall 2023.

Earlier this month, Seagate CFO Gianluca Romano made feedback throughout an investor occasion suggesting that margins and earnings can be “larger than what we guided” highlighting the brand new step in working and monetary momentum.

There’s lots of enthusiasm towards the corporate’s subsequent technology of heat-assisted magnetic recording (“HAMR”) expertise, seen as a breakthrough within the HDD market permitting for larger density, decrease power necessities, and better capability per disk. Administration believes the launch of HAMR merchandise by way of fiscal 2025 may kickstart a brand new spending cycle for patrons seeking to improve as a tailwind for margins.

Individually, the corporate sees a significant alternative to help the information wants surrounding the explosion of generative AI purposes seen as nonetheless within the early phases of improvement and market potential. On this case, as enterprises deploy educated AI fashions, the information storage demand may develop exponentially. From the final earnings convention name:

Over the following a number of years, the amount of AI-generated content material is anticipated to extend and likewise shift in the direction of extra imagery and movies, which could be as much as 1,000 occasions bigger than textual content. These developments bode effectively for HDD demand over the long run, as HDDs stay probably the most cost-effective means to deal with and subsequently use mass capability information.

What’s Subsequent For Seagate?

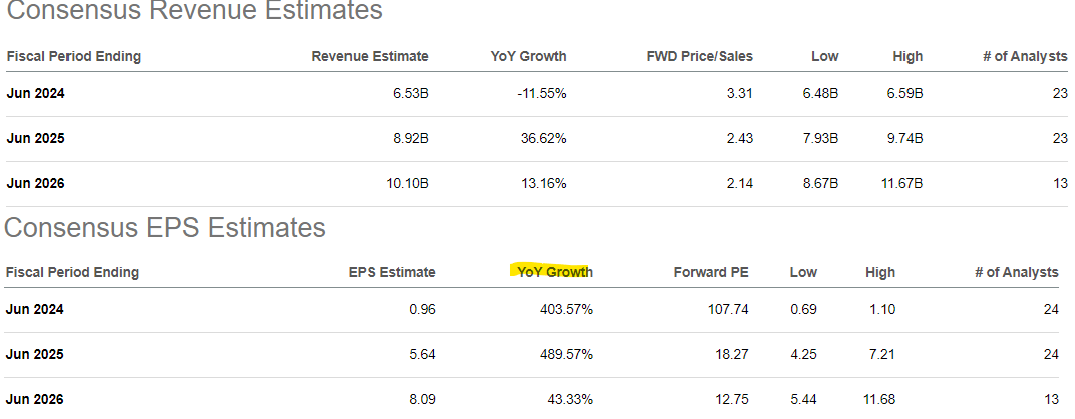

Total, these components play into a robust development outlook as the corporate strikes previous a transitional fiscal 2024. In line with consensus estimates, Seagate’s income development is forecast to climb by 37% subsequent yr and 13% in fiscal 2026. The influence on earnings is much more noticeable with the forecast for 2024 EPS of $0.96, rising to $5.64 by subsequent yr.

In search of Alpha

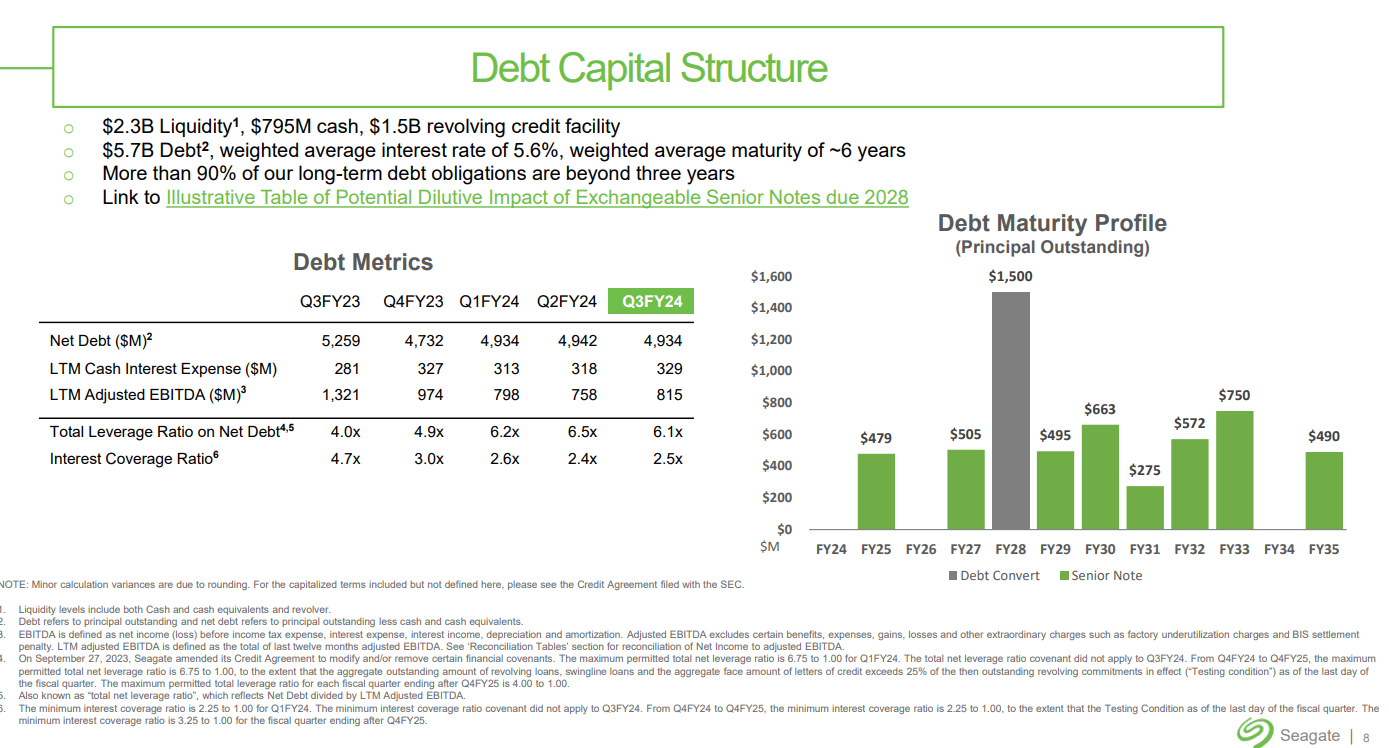

That improved earnings and underlying money circulate ought to go a good distance towards addressing what stays Seagate’s fundamental basic weak point, being its massive internet debt place that ended final quarter at $4.9 billion.

The present internet leverage ratio of 6.1x is elevated however ought to normalize to a degree beneath 3x as earnings ramp up over the following twelve months. Seagate explains that it has restricted debt maturities for the following three years, with ample liquidity to help near-term operations. The corporate’s $0.70 per share quarter dividend yielding 2.7% is sustainable in our opinion.

supply: firm IR

As we see it, the power of earnings to ramp up and a stability sheet de-leveraging to take maintain can characterize a catalyst for shares of STX in its subsequent leg larger.

The inventory is buying and selling at round 18x its fiscal 2025 consensus earnings as a 1-year ahead P/E which even has room to slim in the direction of 13x by fiscal 2025. These ranges are notably enticing for an organization set to generate this degree of worthwhile development.

Last Ideas

We price STX as a purchase with a value goal of $130 representing a 1-year ahead P/E of 23x towards the present fiscal 2025 EPS estimate of $5.64. So long as the corporate continues to execute its monetary turnaround with a restoration to the HDD market, the upside right here is for an enlargement in valuation multiples.

When it comes to dangers, we acknowledge that Seagate stays uncovered to broader developments within the expertise sector and sentiment in the direction of themes like cloud computing and even synthetic intelligence. A situation the place international macro circumstances deteriorate may pressure a reassessment of the earnings outlook and open the door for a deeper selloff.

Monitoring factors over the following few quarters embody the evolution within the gross margin and the mass-capacity storage market.