Regeneron: Downgrading My Outlook To ‘Maintain’ Forward Of Q2 Earnings (NASDAQ:REGN)

serggn/iStock by way of Getty Pictures

Funding Overview: Regeneron Recap Illustrates Excessive Valuation, Justified By Excessive Potential

I final lined the Watertown, Massachusetts “Massive Pharma” concern Regeneron Prescription drugs, Inc. (NASDAQ:REGN) in a be aware for Looking for Alpha in January, titled “Why I Count on Regeneron To Preserve Delivering For Traders In 2024 (Improve).”

At the moment, Regeneron shares had been value $895 per share. Whereas making the purpose that by some metrics – price-to-sales, price-to-earnings, comparisons towards different “Massive Pharma” corporations – Regeneron inventory was priced at a premium, my analysis – utilizing detailed pipeline and product income forecasts, earnings assertion modelling, and discounted money move evaluation – instructed a worth goal of >$1,000 per share was not unrealistic.

So it has confirmed thus far in 2024 – Regeneron inventory is up >20% year-to-date, and shares commerce at a price of $1,071 on the time of writing.

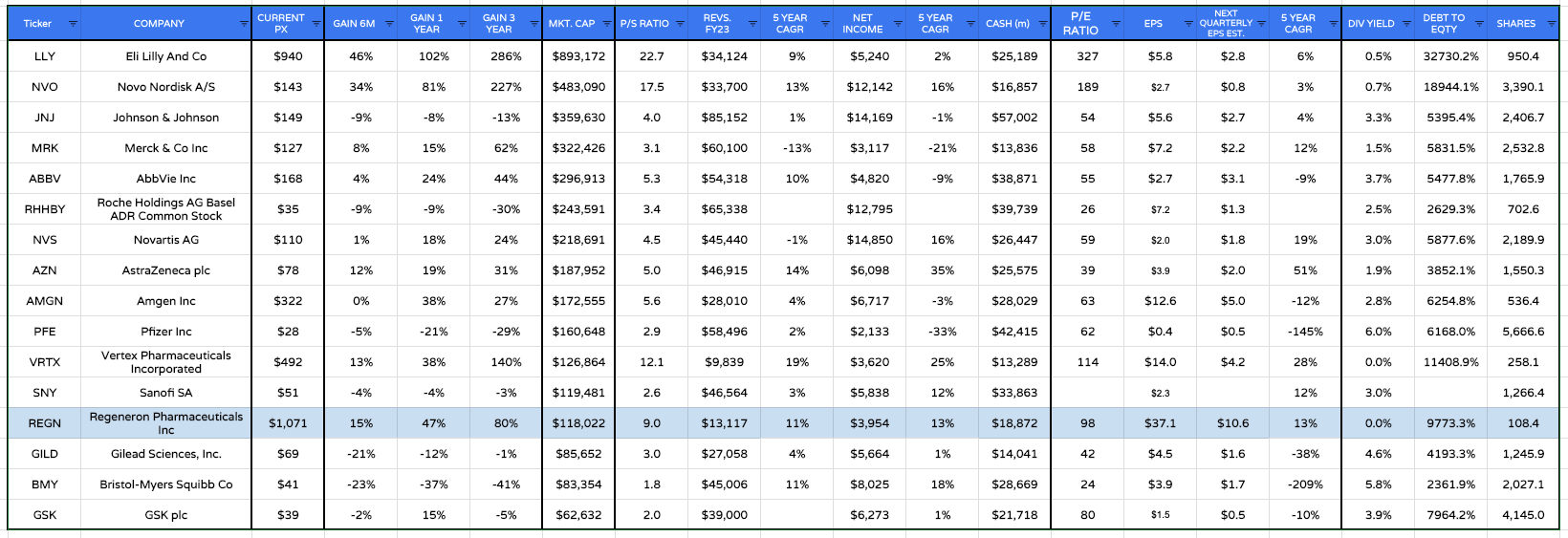

Regeneron in comparison with international Pharmas (my desk utilizing knowledge from TradingView, Google Finance)

If we think about the desk above, we are able to see that Regeneron’s present market cap of $118bn makes it the thirteenth largest Pharma within the US and Europe by valuation. Nevertheless, it’s the fifteenth largest by income, with Gilead Sciences, Inc. (GILD), in fourteenth place, incomes greater than twice as a lot income in 2023 as Regeneron.

Regeneron has the fourth-highest price-to-sales ratio – 9x – and the fourth-highest price-to-earnings ratio – 98X – which means that the market is both overvaluing the inventory or expects to see industry-beating progress from the corporate. If we think about Regeneron’s spectacular 5-year CAGR progress – the fourth greatest within the sector – then the latter argument appears legitimate.

Regeneron additionally boasts present belongings of almost $19bn, with >$10bn held in money, towards ~$3.6bn of present belongings (as of the conclusion of Q1 2024), and whole liabilities of $7.4bn. When it comes to share worth efficiency, on a 3-year foundation, Regeneron is the fourth-best performer, up 80%, and the third-best performer on a 1-year foundation, and on a 3-month foundation.

In abstract, there’s a lot to love about Regeneron as an funding alternative. Nevertheless, it is also vital to notice that a lot of Regeneron’s valuation relies on its potential – what the market believes it may do going ahead – relatively than efficiency – what the corporate is doing within the current.

Underneath The Hood – What Makes Regeneron Stand Out As A Promising Pharma Funding?

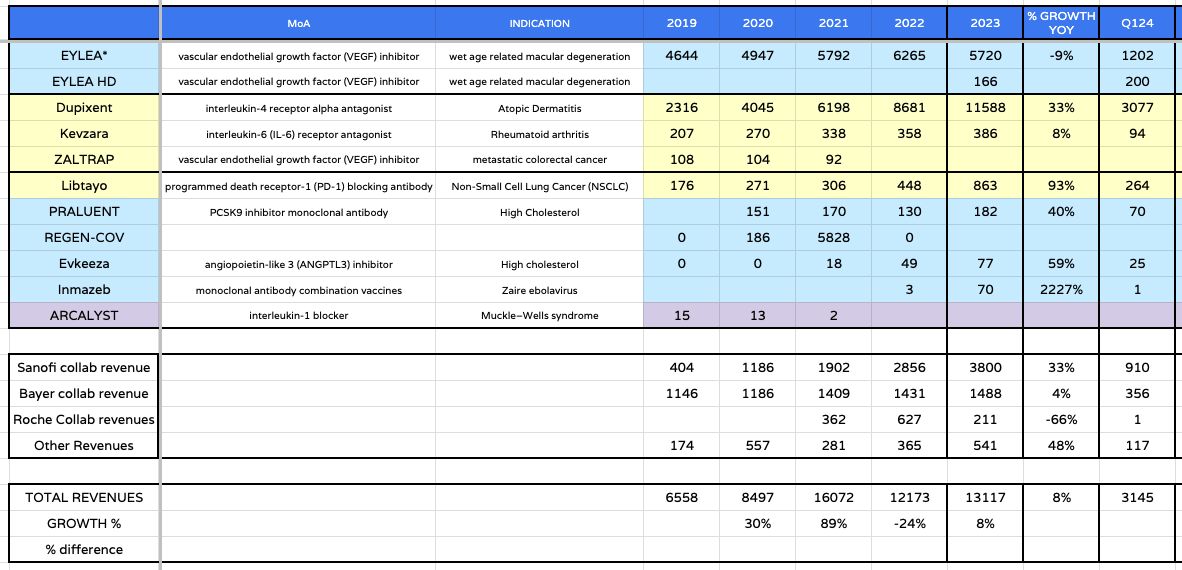

The beneath desk gives an illustration of Regeneron’s present product portfolio and revenues over the previous few years, together with 2023, and Q1 2024 efficiency.

Regeneron product portfolio (my desk utilizing firm figures)

It’s instantly clear that the principle income drivers are Eylea, a VEGF-inhibitor accredited to deal with eye illness moist superior macular degeneration, and Dupixent, an IL-4 receptor antagonist indicated to deal with atopic dermatitis and different inflammatory autoimmune situations.

It is important to notice that the figures quoted above for Eylea are primarily based on US gross sales solely. The drug is marketed and offered in Europe by German Pharma Bayer, who pay Regeneron collaboration revenues, which will be seen decrease within the desk.

Equally, the Dupixent, Kevzara, and Zaltrap revenues proven above relate to whole revenues earned by Regeneron’s accomplice Sanofi (SNY), the French Pharma – Regeneron’s share of these revenues is quoted within the “Sanofi collab income” row, beneath.

What’s vital is that we are able to see the significance of Eylea and Dupixent to Regeneron’s enterprise, and may see the exceptional progress of Dupixent into one of many world’s best-selling medicine.

At first of July, Sanofi (SNY) and Regeneron introduced that Dupixent has been accredited by the European Medicines Company (“EMA”) in a brand new indication, Power Obstructive Pulmonary Illness (“COPD”). The drug could possibly be accredited for a similar indication within the US earlier than the tip of the yr.

Dupixent has been pegged by analysts to attain peak revenues of >$20bn every year, and with Regeneron’s share of revenues ~30%, this must be a wholesome supply of rising revenues for the corporate for a few years to return.

In the meantime, as we are able to see from the desk above, Regeneron’s US Eylea gross sales fell year-on-year in 2023, from ~$6.3bn to $5.7bn. As I wrote in my January be aware:

Eylea has typically been the “greatest in school” or “normal of care” drug in its indication all through its life as a business product, resisting a number of challenges from merchandise launched by the likes of Swiss Pharmas Roche Holding AG (OTCQX:RHHBY) and Novartis AG (NVS), however Roche’s newest product, Vabysmo – a bispecific antibody that targets each vascular endothelial progress issue (VEGF) and angiopoietin-2 (Ang-2) – has been proven in research to have a longer-lasting impact, and the drug has been taking market share away from Eylea in 2023.

Regeneron already has an answer to its Vabysmo downside, having secured approval final yr for Eylea HD, an 8mg injection with 12- and 16-week dosing regimens, towards normal Eylea’s 8-week dosing regime. With this approval, Regeneron has rapidly been capable of re-take best-in-class standing from Roche and Vabysmo

Vabysmo earned ~$2.7bn of revenues in 2023, whereas Eylea revenues fell 9% year-on-year, nonetheless, we are able to see that in Q1 2024, gross sales of Eylea HD had been increased than throughout the entire of 2023. With that mentioned, nonetheless, Vabysmo revenues in Q1 2024 had been up >100% year-on-year, reaching >$925m, so it’s clear that Regeneron faces intense competitors in its most trusted market.

As such, I might sound a cautious be aware on the long-term efficiency of Eylea and Eylea HD. I might not essentially count on to see revenues rising year-on-year going ahead. Nevertheless, I might not count on them to fall considerably, both – Regeneron has an excessive amount of expertise on this market.

The opposite success story in Regeneron’s portfolio is Libtayo, a PD-1 blocking antibody accredited to deal with non-small cell lung most cancers (“NSCLC”) and cutaneous squamous cell carcinoma (“CSCC”). The drug has an analogous mechanism of motion to Merck & Co., Inc.’s (MRK) all-conquering most cancers drug Keytruda, which earned >$25bn of revenues final yr.

Libtayo revenues grew by 45% year-on-year in Q1 2024, to $264m, implying the drug will grow to be a “blockbuster” in 2024. It might be unrealistic to count on Libtayo to match the income efficiency of Keytruda. Nevertheless, Regeneron is testing the drug alongside a number of of its pipeline belongings, similar to its LAG-3 inhibitor fianlimab, in metastatic melanoma. Pivotal examine outcomes are anticipated in 2025, and its PSMAxCD28 bispecific REGN5678, in prostate most cancers, and its MUC16xCD3 bispecific ubamatamab, in ovarian most cancers.

As I’ve written in earlier notes on Regeneron, administration has a helpful knack for delivering when it counts. Subsequently, though the corporate has not had nice publicity to oncology markets up to now, with it rising as the first focus going ahead, that is most likely the house to observe most intently.

If administration is as profitable on this discipline because it has been within the ophthalmology and autoimmune markets, I believe there could also be a double-digit billion income alternative in play, long-term. Nevertheless, Regeneron will likely be going it alone with Libtayo, having bought full rights to the drug from Sanofi in 2022.

Wanting Forward – Does Regeneron Nonetheless Warrant A “Purchase” Advice After Posting Sturdy Beneficial properties In 2024 To Date?

That is the important thing query for shareholders and traders to reply. In Q1 2024, Regeneron reported revenues of $3.145bn, which was a slight year-on-year decline of ~1% and GAAP internet earnings additionally declined, by 12%, to $722m, whereas internet earnings per share (“EPS”) fell to $6.27, from $7.17 within the prior yr interval.

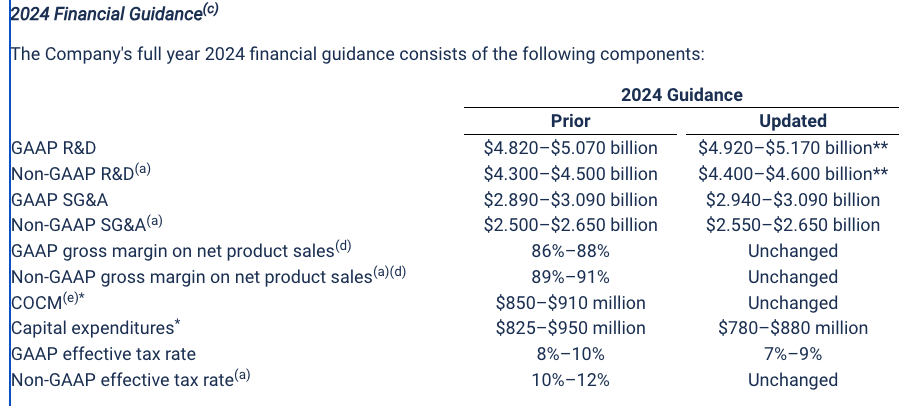

Regeneron doesn’t usually present ahead income steering, which complicates issues. Nevertheless, the corporate does break down bills, as proven beneath:

Regeneron 2024 steering (Q1 24 earnings press launch )

If we add GAAP R&D, SG&A, and capital expenditures we get near ~$9bn, plus a tax price of ~8%. My expectation is that Regeneron will ship within the area of ~$13.5bn of revenues in 2024, round a 3% annual uplift, and subsequently I might count on EPS in 2024 to be broadly much like, or a smidgen decrease than in 2023, ~$35.

If I subsequently repeat the identical train I carried out in my final be aware and share longer-term income projections for merchandise and pipelines, a forward-looking earnings assertion projection, and a reduced money move evaluation, it must reply the query. That’s, whether or not Regeneron inventory has additional upside to understand. So, right here goes.

Firstly, I am going to share my income projections as follows:

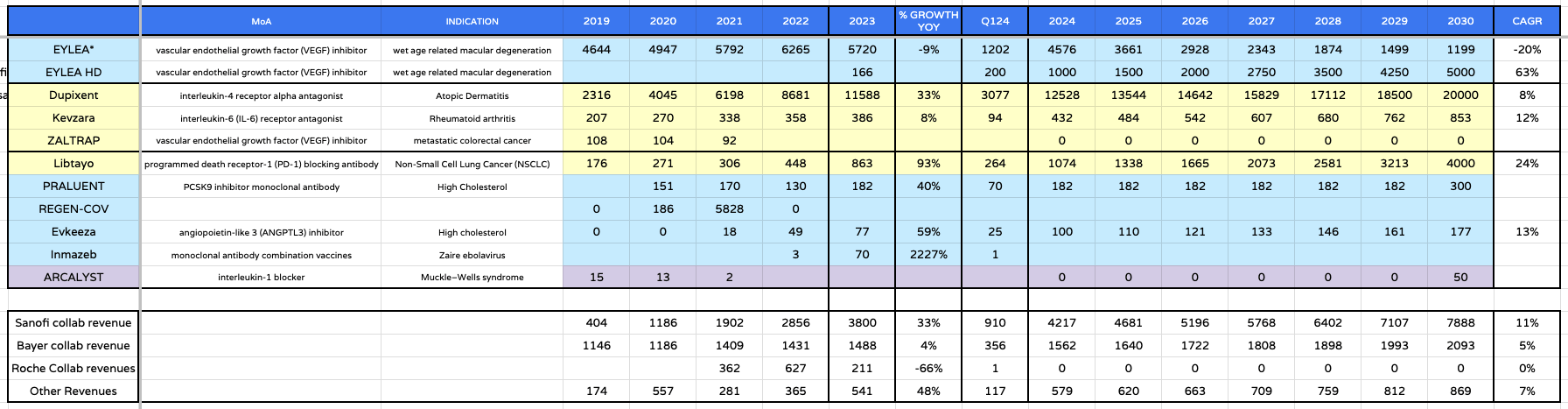

Regeneron – ahead income projections (my desk and assumptions primarily based on mgmt. steering)

As mentioned above, my expectation is that Dupixent meets the market’s >$20bn peak income expectations, growing Regeneron’s share of revenues from that supply to shut to ~$8bn. Alternatively, even with Eylea HD offsetting Eylea losses, I do not see main progress from this supply, however neither do I forecast heavy losses.

I’m forecasting that Libtayo turns into successful story within the immune checkpoint inhibitor (“ICI”) house, reaching peak revenues of ~$4bn, however I’m much less optimistic in regards to the future prospects for the ldl cholesterol franchise.

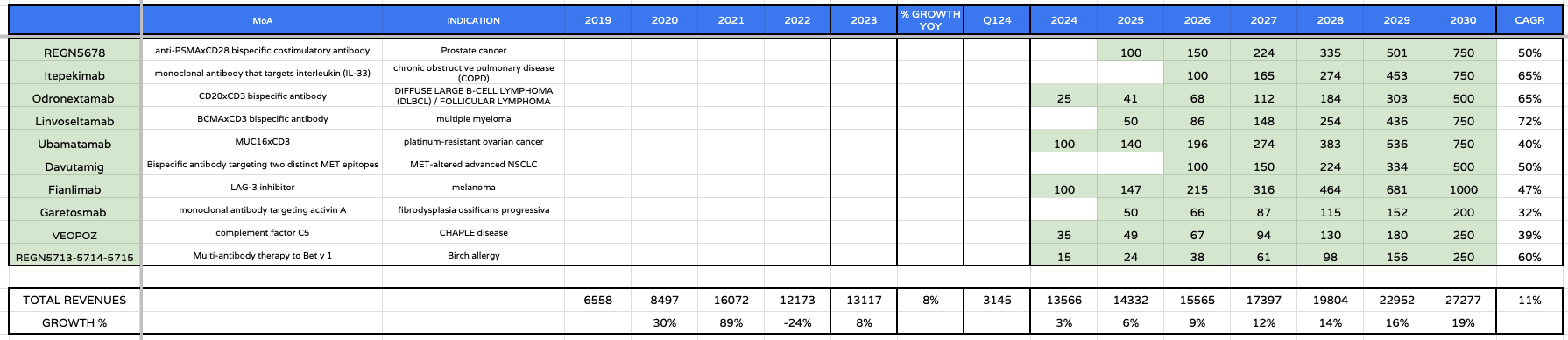

pipeline prospects (my desk and projections)

Turning to Regeneron’s pipeline, as talked about, there are a number of oncology belongings which will work properly in combo with Libtayo, though my predictions for revenues from these sources in 2024 could also be unrealistic, and require adjustment going ahead. Linvoseltamab has a PDUFA date (when the FDA broadcasts whether or not the drug has received approval) of August twenty second, in melanoma, however odronextamab obtained a rejection in follicular lymphoma and diffuse massive B-cell lymphoma (“DLBCL”) in March. Altogether, by 2030, nonetheless, I see Regeneron’s pipeline doubtlessly contributing almost $6bn to the highest line.

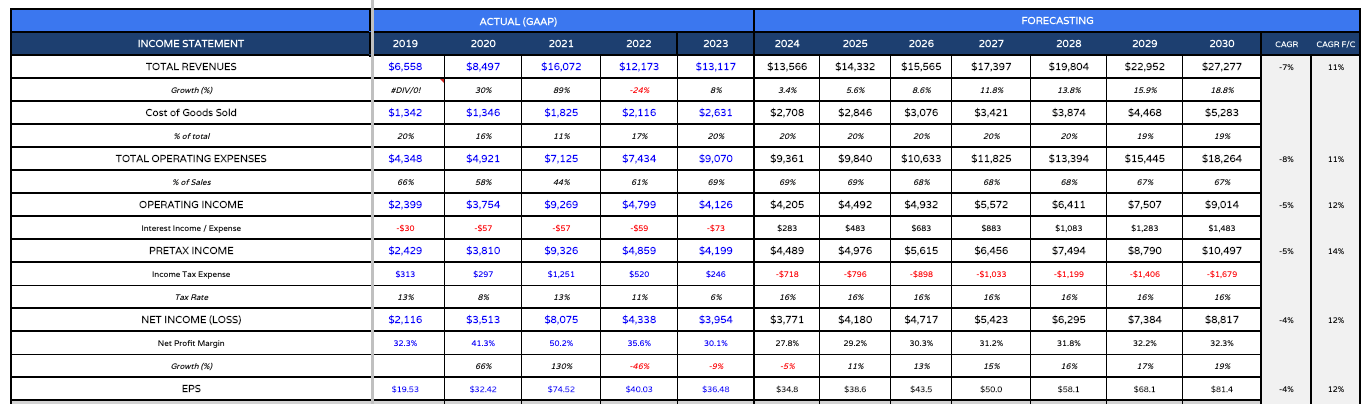

Revenue assertion forecast (my desk and assumptions primarily based on historic knowledge)

When it comes to my earnings assertion forecast, as mentioned, I don’t see a lot progress in 2024. In an in any other case optimistic state of affairs, operational prices ease barely, and internet earnings and EPS improve yearly, with EPS greater than doubling by 2030.

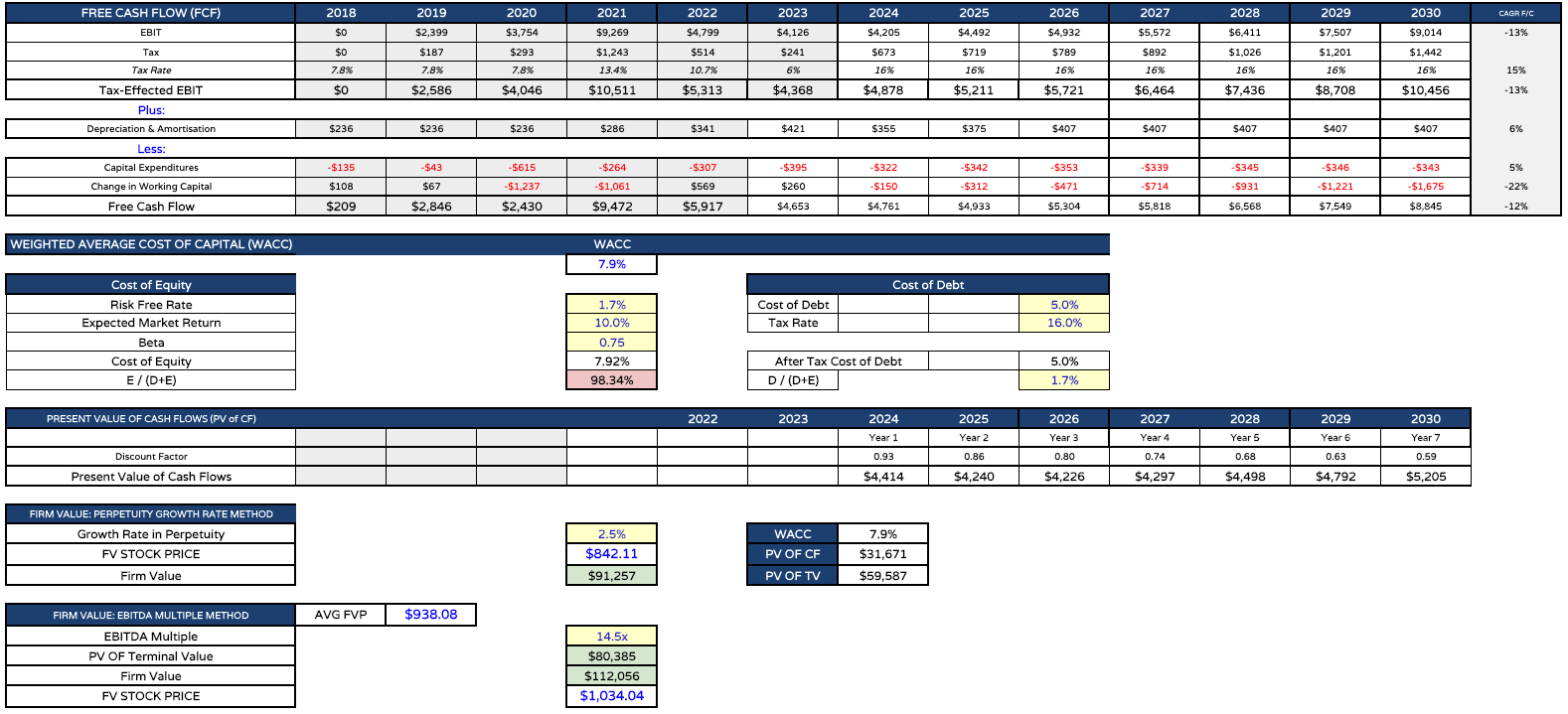

Lastly, I am going to current my discounted money move (“DCF”) evaluation and current my share worth “honest worth” determine.

Regeneron (my desk and assumptions)

As we are able to see above, my revised worth goal for Regeneron inventory is $842 on a perpetuity progress technique, and $1034 on an EBITDA a number of foundation, for a mean of $938.

That is kind of the identical because the determine I bought in January, though the weighted common value of capital used on this occasion is simply 7.9%, relatively than the determine of 8.6% I utilized in January. If I used this determine at the moment, the share worth goal can be nearer to $910.

I’ve been a bit extra conservative with some ahead estimates and a bit stricter with operational bills as a proportion of revenues (to match my calculated EPS forecast). All issues thought-about, I might say I’m rather less bullish on Regeneron than I used to be, primarily based on a couple of elements. These embody the brand new competitors for Eylea, the shortage of progress in Q1, a few pipeline setbacks, the risk posed by the brand new GLP-1 agonist drug class to Regeneron’s cholesterol-lowering franchise, and fewer optimism round Regeneron’s skill to cut back prices and enhance margins (primarily based on firm steering for 2024).

As such, I’ll downgrade my “Purchase” suggestion to a “maintain” suggestion. Given Regeneron doesn’t pay a dividend, I might not make the corporate a stand-out funding alternative within the “Massive Pharma” sector right now. Nevertheless, that is on no account an underperforming firm, however relatively a sufferer of its success lately.

I’ve persistently suggested traders to look out for worth dips. As long as the rationale for the dip is macroeconomic relatively than company-specific, think about shopping for, as administration does have the knack of pulling rabbits out of hats and the subsequent earnings launch is scheduled for August 1st.

There may be loads of promise remaining within the pipeline. Presently, nonetheless, I do not see compelling explanation why the Regeneron Prescription drugs, Inc. inventory worth would breeze previous the $1,100 mark, however relatively a couple of indicators {that a} small correction could possibly be within the offing.