Integer: Value/Worth Equation Stays Impartial – Reiterate Maintain (NYSE:ITGR)

Pgiam/iStock by way of Getty Photographs

Funding Abstract

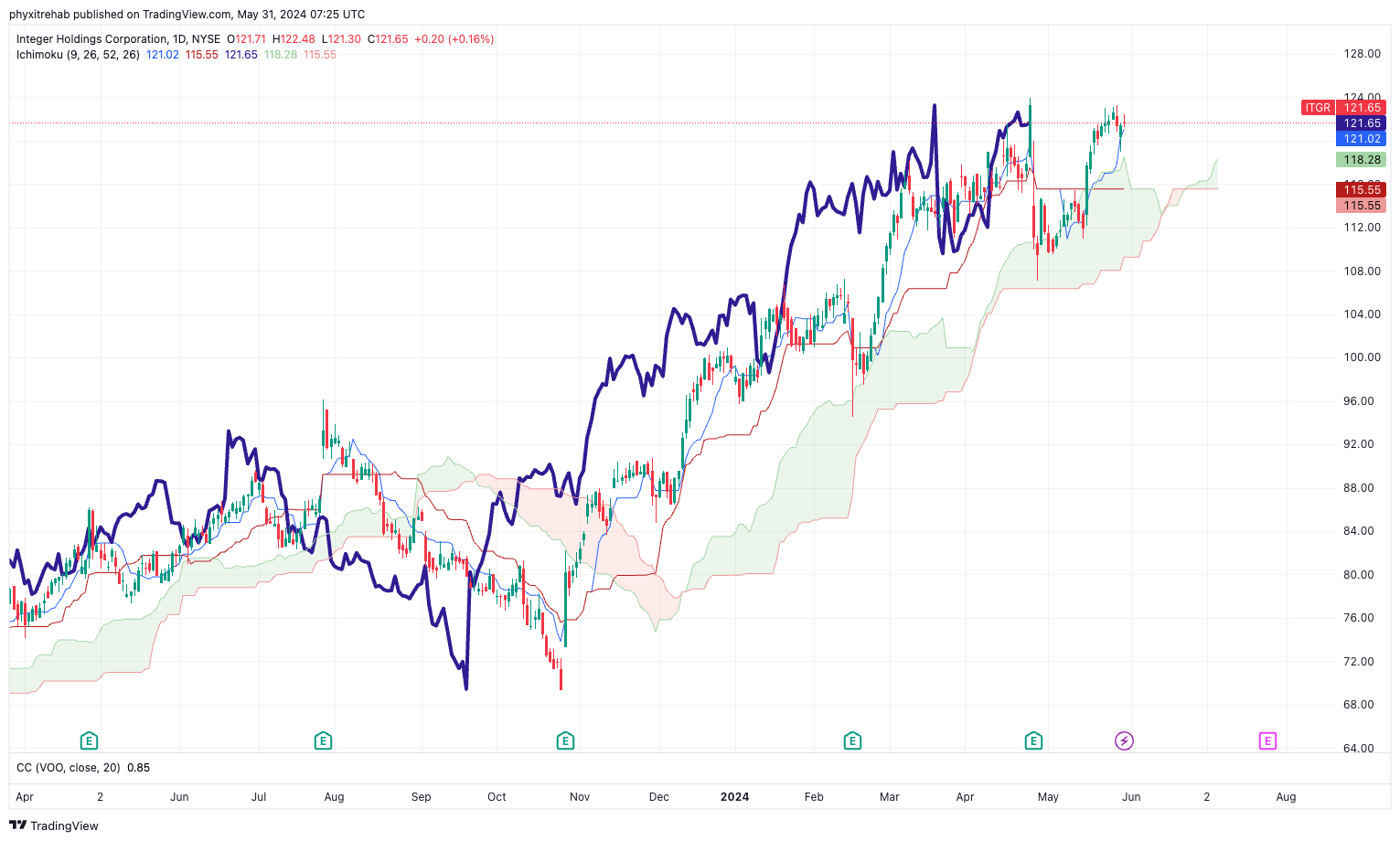

Since my final report on Integer Holdings Company (NYSE:ITGR), the inventory has skilled a considerable re-rating, surging practically 60% from my earlier maintain name. This spectacular progress has propelled the inventory from a modest base of round $90/share to $121/share as I write.

Determine 1.

Tradingview

There is no such thing as a denying buyers have bid up the corporate’s inventory worth and earnings multiples because the final publication. My questions now are threefold: 1) What might I’ve missed? 2) What’s driving the change in market worth? and three) Has the market bought it proper?

Right here I’ll run by the solutions to every of those questions right this moment and hyperlink again to the broader funding debate for ITGR. Regardless of the good points in share worth, my estimates nonetheless arrive on the conclusion of a maintain on this firm. This report will run by my the explanation why. That isn’t to say that (i) I’m in any respect right, or that (ii) ITGR inventory received’t proceed to realize sooner or later. However, primarily based on our first-principles funding pondering right here at Bernard, there’s a misalignment to what we will comfortably allocate to the corporate. Internet-net, I proceed to charge ITGR a maintain for causes outlined on this report.

Q1 FY’24 earnings decomposition

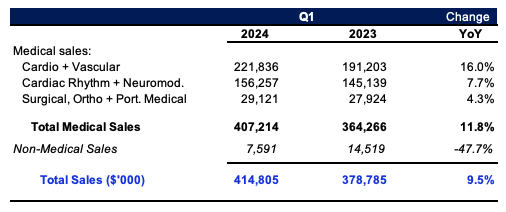

ITGR grew gross sales 10% yr over yr in Q1 ‘24 to $415 million, with c.600 foundation factors of this delivered by the underlying enterprise. It pulled this to adj. working earnings of $63 million, up 26% on final yr, and earnings of $0.20 per share, down from $0.59 the yr prior.

Administration revised up FY’24 full yr steerage following the robust quarter. It now eyes 9–11% high line progress this yr, calling for $1.77 billion in revenues on the higher finish (up 200 foundation factors from earlier). It’s trying to adj. EBITDA on this of $375 million on the high finish of vary, and would possibly clip earnings of $171-$185 million, up 8–18% if it does happen. Lastly, administration appears to take a position round $110 million to capital expenditures for the yr (6.2% of est. gross sales; $3.28/share).

The divisional breakdown was as follows:

- Cardio & vascular gross sales have been up 16% yr over yr to clip $221.8 million. Administration mentioned demand was robust throughout all of the phase’s markets, with upticks in electrophysiology and structural coronary heart purposes.

- Cardiac rhythm administration and neuromodulation gross sales grew 770 foundation factors over the yr to $156.2 million. There have been no main progress drivers talked about by administration within the phase in the course of the quarter. Progress was robust nonetheless in my goal view.

- The surgical orthopaedic and moveable medical enterprise was up 4% % on the yr and put up $29.1 million in revenues. As a reminder, administration are exiting the moveable medical enterprise over the following few years.

Determine 2.

Firm filings

In my opinion this was a fairly robust quarter from ITGR and progress numbers have been above historic vary. For example, final 12 month gross sales progress of 13% is above the corporate’s 5 yr common of 5.5%, and practically double the sector median of seven%.

Consensus expects robust progress charges from the corporate transferring ahead as properly. It initiatives 31.6% ahead progress in pre-tax earnings this yr, off gross sales progress of 10% in 2024, according to administration forecast. Wall Avenue is eyeing 13 to 14% backside line progress over the approaching two years respectively.

With this type of high and backside line momentum constructing for ITGR, it will be unwise to not make revisions to my modelling, which I talk about under.

Backdrop of fundamentals

In my final two publications on the corporate, I’ve spent intensive time illustrating its core fundamentals, enterprise traces, key dangers, business outlook, and rivals. (You may verify my evaluation on the corporate from August + February 2023 by clicking right here, and right here respectively). I’m going to piece just a few extra of the transferring components of the funding debate collectively for the advantage of our readers right this moment.

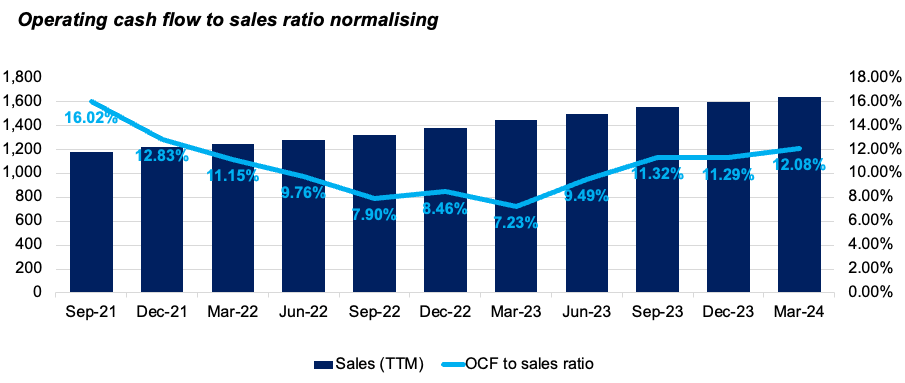

As seen in Determine 3, gross sales have been rising at an inexpensive clip every interval on a rolling 12 month foundation since 2021. The working money circulation to gross sales ratio, measured because the rolling 12 month money from operations in opposition to gross sales, noticed important contraction throughout the 2021 to 2023 interval. It fell from 16% of income to round 7% in Q1 2023. One potential standout is that, as revenues have continued their advance, so who has the quantity of working money circulation the corporate has realized. The ratio is subsequently normalising to a long-term vary of 12% to 14% %.

Determine 3.

Firm filings

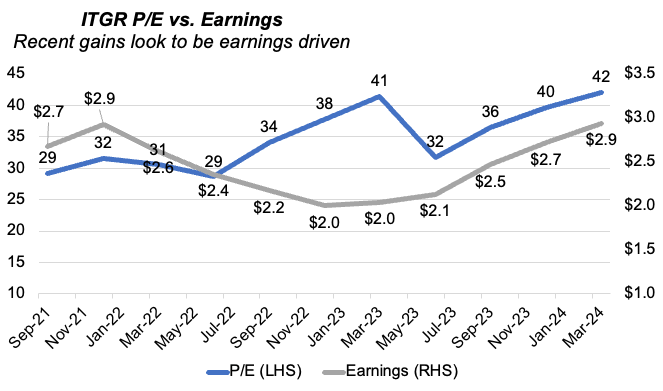

As to what’s driving the change in market worth, it will seem that it is a mixture of each earnings progress and alter within the P/E a number of.

Determine 4 tracks the corporate’s P/E a number of and rolling earnings per share on a 12 month foundation since 2021. As seen, there was a big dislocation in worth (P/E) relative to earnings all through 2022 and 2023, However since administration has grown quarterly earnings from $2.00 per share as much as $2.90 per share in final 12 months, buyers have continued to bid up the next earnings a number of as properly. On the time of publication, the corporate trades at 42x trailing GAAP earnings, and 24.6x trailing non-GAAP earnings.

So it means that 1) administration are rising earnings, and a pair of) buyers are paying larger greenback values for one greenback of these earnings.

Determine 4.

BIG Investments, firm filings

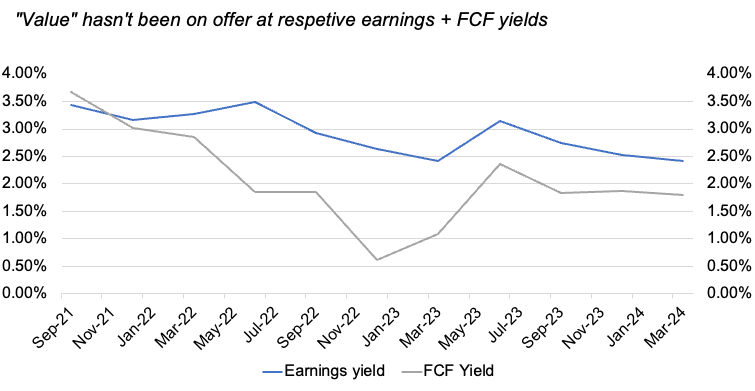

The worth investor’s have obtained from any such exuberant exercise will not be famous in Determine 5. The respective earnings and free money circulation yields have been reducing steadily since 2021, regardless of no apparent change within the firm’s market worth till 2024. Buyers have paid the respective P/E multiples proven above, realising reducing yields of round 100 foundation factors on earnings, and practically 350 foundation factors on free money circulation.

Critically, I can say that I’ve not missed any components of the basic story, or the expansion story. I’m simply at odds with how the market has priced this firm within the final six months.

Determine 5.

Bloomberg, BIG Investments

Outcomes of modelled situations

I discussed consensus progress estimates earlier. These aren’t unreasonable figures for my part, particularly given 1) the latest gross sales progress the corporate has exhibited, and a pair of) uptick in progress within the cardio and vascular enterprise, pushed largely by gross sales of its submit subject ablation (“PFA”) gadgets.

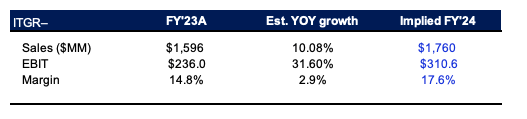

If administration have been to hit the estimated progress of 10% in gross sales + 31-32% progress in pre-tax earnings this yr, this might suggest a pre-tax earnings margin of 17.5%. (That is roughly 300 foundation factors above 2023).

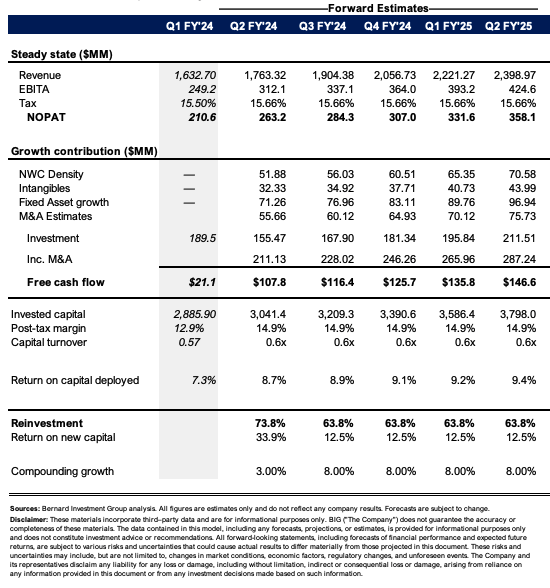

This can’t be neglected. Enterprise returns – that’s, returns on present and incremental capital – are pushed by the mix of working margins (post-tax), and turnover of gross sales on invested capital. ITGR doesn’t get pleasure from beneficial economics on this regard for my part. Put up-tax margins of round 13% produced on capital turnover of 0.6x leads to a return of seven.3%. That is in step with the common 7% ROIC administration has produced over the past three years every interval.

A rise of working margin to the 17% degree mixed with added gross sales progress might be a constructive inflection level on its share worth. I’ve subsequently bought to get some scope on what this might imply for the corporate going ahead.

Determine 6.

In search of Alpha, BIG Investments

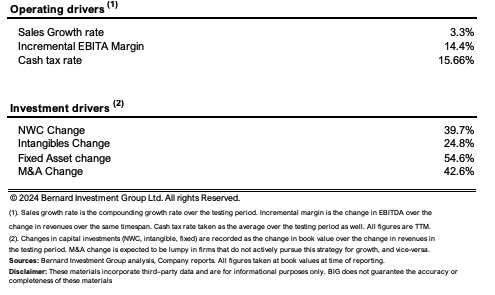

Determine 7 depicts administration’s capital allocation choices over the previous three years alongside the monetary outcomes of the enterprise. It does this on a rolling 12 month foundation. Gross sales have grown at round 3.3% every interval, with pre-tax margins of 14.4%. To provide a greenback of gross sales progress, administration has needed to make investments $1.19, or $1.60 together with all acquisition exercise. That is distributed throughout all areas of capital. For example, it required $0.40 on the greenback of funding to working capital and round $0.55 of funding towards fastened property to provide an incremental $1.00 of income.

Determine 7.

Firm filings

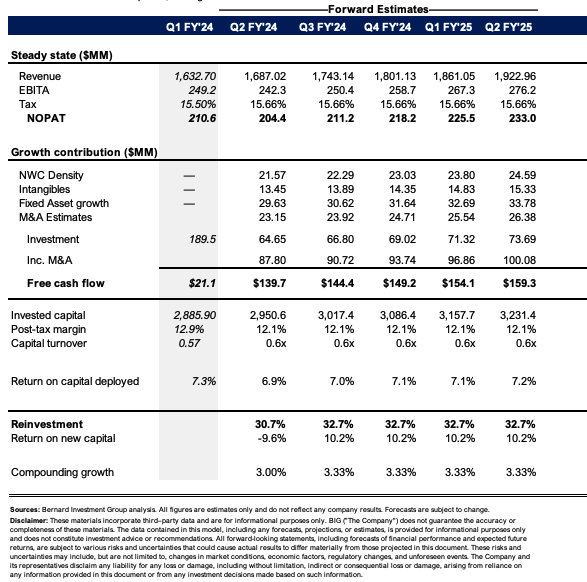

If administration have been to proceed alongside these traces, with out deviating too removed from latest historical past, my estimates challenge the corporate may do roughly $1.7 billion in gross sales in 2024, and round $1.92 billion in 2025. That is according to consensus estimates. I’d additionally name for pre-tax earnings of $250 million this yr, stretching as much as $278-$280 million the next yr. This might lead to robust free money circulation manufacturing of round $100 million-$150 million underneath these assumptions. Administration initiatives round $105 million in free money circulation this yr.

If this have been the case, as I mentioned in my valuation factors later, this isn’t a pretty proposition to us.

Determine 8.

BIG Investments

The Query: how do the perceived modifications in outlook change the funding debate, if in any respect? Right here, I’m going to hold an 8% common progress charge going ahead, and an incremental pre-tax margin of 17%. These are according to my estimates and mirror Wall Avenue’s view as properly.

The modifications are fairly drastic. I get the corporate at $1.7 billion – $1.9 billion in gross sales this yr, stretching to $2.4 billion by 2025 on pretax earnings of $424 million. It may nonetheless spit off $100 million-$150 million underneath these assumptions, because of the upper progress charge and working margin feeding more money down the P&L and to shareholders on the finish of the day or for reinvestment.

As I’ll talk about under, this has fairly a considerable change on valuation, however, critically, not sufficient for me to imagine it’s undervalued.

Determine 9.

BIG Investments

Valuation

Because it pertains to valuation ITGR presently trades at 24x coaching earnings as talked about earlier. It additionally sells at round 27x trailing EBIT. Each of those multiples are giant premiums to the sector of 27% and 20% respectively.

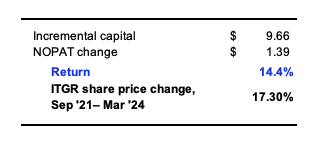

My query from earlier was, has the market bought it proper. To this, I’m first going to see if it’s got it proper up till date. For this, I benchmark the corporate’s incremental return on capital, multiplied by the quantity reinvested at these charges, after which examine this to the full change in share worth since Q3 2021. That is on a rolling 12 month foundation.

Over this time, administration has invested an incremental $9.60 per share again into the enterprise to engender an extra $1.40 per share of submit tax earnings, in any other case 14.4% incremental return on funding. Over the identical time, the ITGR share worth climbed by 17.3%, proper earlier than the breakout on the finish of Q1 2024. In my opinion, the market had priced the corporate accurately up till this level, and this was mirrored in my prior analyses.

Determine 10

Bernard Investments

Now the stakes at the moment are completely different and clearly there may be extra optimism priced into the inventory at its present ranges. I’m going to deal with this in various methods.

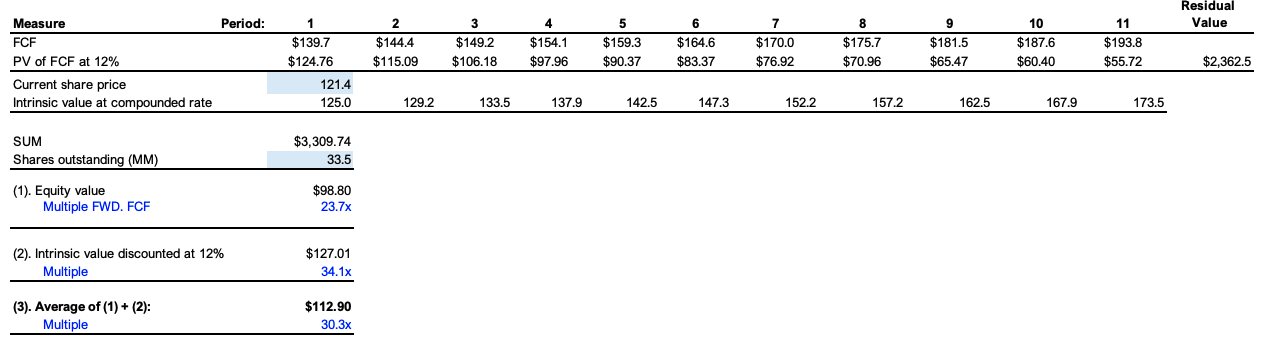

First, I’m going to challenge my estimates of free money circulation out over the approaching 10 years, on the adjusted charge of progress and margin. I then low cost this again at a charge of 12%, reflecting the chance value of the long-term market averages. I mix this with a mannequin that compounds the valuation on the operate of return and invested capital and reinvestment charge (ROIC x reinvestment charge).

Doing so, I get to a blended valuation of $113 per share, under the place the corporate trades right this moment as as I write. That is supportive of a impartial view, with the revised progress assumptions baked in.

Determine 11.

BIG Investments

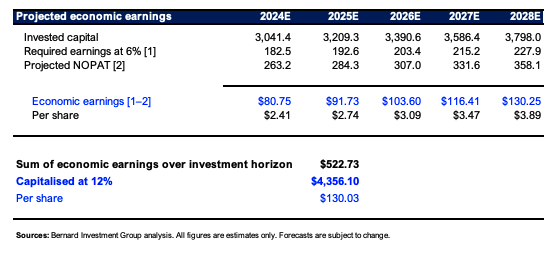

Secondly, I desire a good understanding of how economically priceless these earnings and money flows really are to us relative to a chance value. To be economically priceless, the submit tax earnings must be produced at a charge above 6% invested capital transferring ahead. That is according to the present beginning yields on most funding grade corporates. Something above this stipulated determine can be thought of economically priceless. For example this yr, it will want $182.5 million in submit tax earnings as a way to hit this threshold. My numbers challenge it may do $263 million on the new progress and margin charges, resulting in “financial revenue” of $80.75 million, $2.41 per share. I then sum these projections from the following 5 years, and low cost them on the 12% whole charge from earlier than.

I get to a valuation of $130 per share doing this, marginal upside on right this moment’s values. What this implies is that the financial earnings I’d hope to strip out of this firm over the approaching 5 years, when capitalised on the 12% charge, solely quantity to a determine roughly $9 per share above the place it trains right this moment. This isn’t sufficient margin of security to get us right here, even with the revised progress and margin assumptions.

Determine 12.

BIG Investments

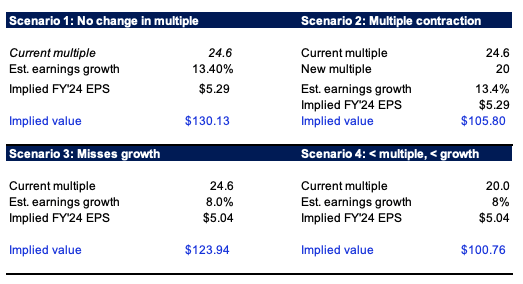

Lastly, I needed to run by various situations to see what would occur if the excessive multiples have been to contract, or if progress numbers weren’t hit. As seen under, if administration does hit consensus progress estimates of 13.4% in EPS this yr, and there’s no change within the P/E a number of, the inventory can be value round $130 to us right this moment – precisely the place I get to when contemplating my revised estimates. If the a number of have been to contract again to 20x, and it nonetheless hits the expansion numbers, then the inventory can be value $105 to us right this moment, illustrating how delicate it’s to a contraction in multiples. Equally if it misses progress and prints 8% growth on the backside line this yr, this will get us to $123 per share, marginally above the place we commerce as I write. So even when buyers do pay that a number of, and it misses, it could be pretty valued. It’s all within the a number of, and never essentially within the fundamentals in my view.

Determine 13.

BIG investments

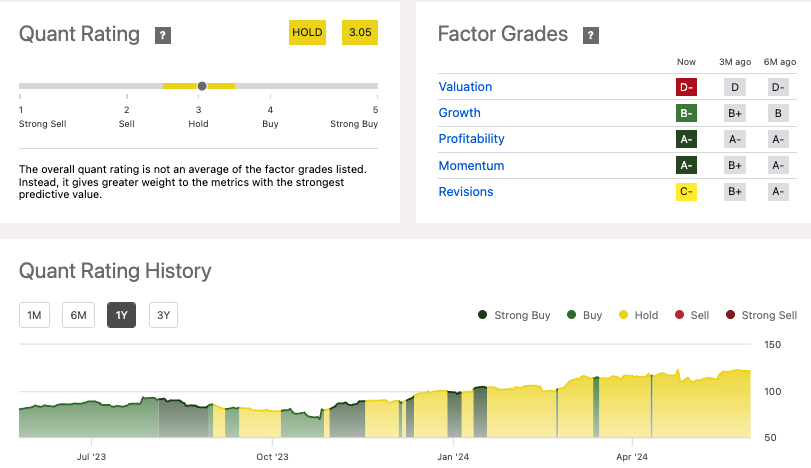

In consequence, similar to the In search of Alpha quant system proven under, I’m reiterating my stands on ITGR as a maintain on grounds of financial worth and valuation.

Determine 14.

In search of Alpha

Conclusion

Buyers proceed to pay excessive multiples for ITGR. This has led to a considerable repricing in its market worth since my final publication. Nevertheless, I can not wrap my head round paying greater than 40 instances reported earnings, with trailing returns of capital of seven%, and an absence of financial worth to be drawn from this identify primarily based on my evaluation. From the end result of those views, I reiterate my stance on the corporate as a maintain and look ahead to offering additional updates.