Danske Financial institution: Important Capital Returns Forward (OTCPK:DNSKF)

Ole Schwander

Danske Financial institution A/S (OTCPK:DNSKF) has reported a optimistic working efficiency in Q2, plus its extra capital place permits it to distribute important dividends over the subsequent couple of years.

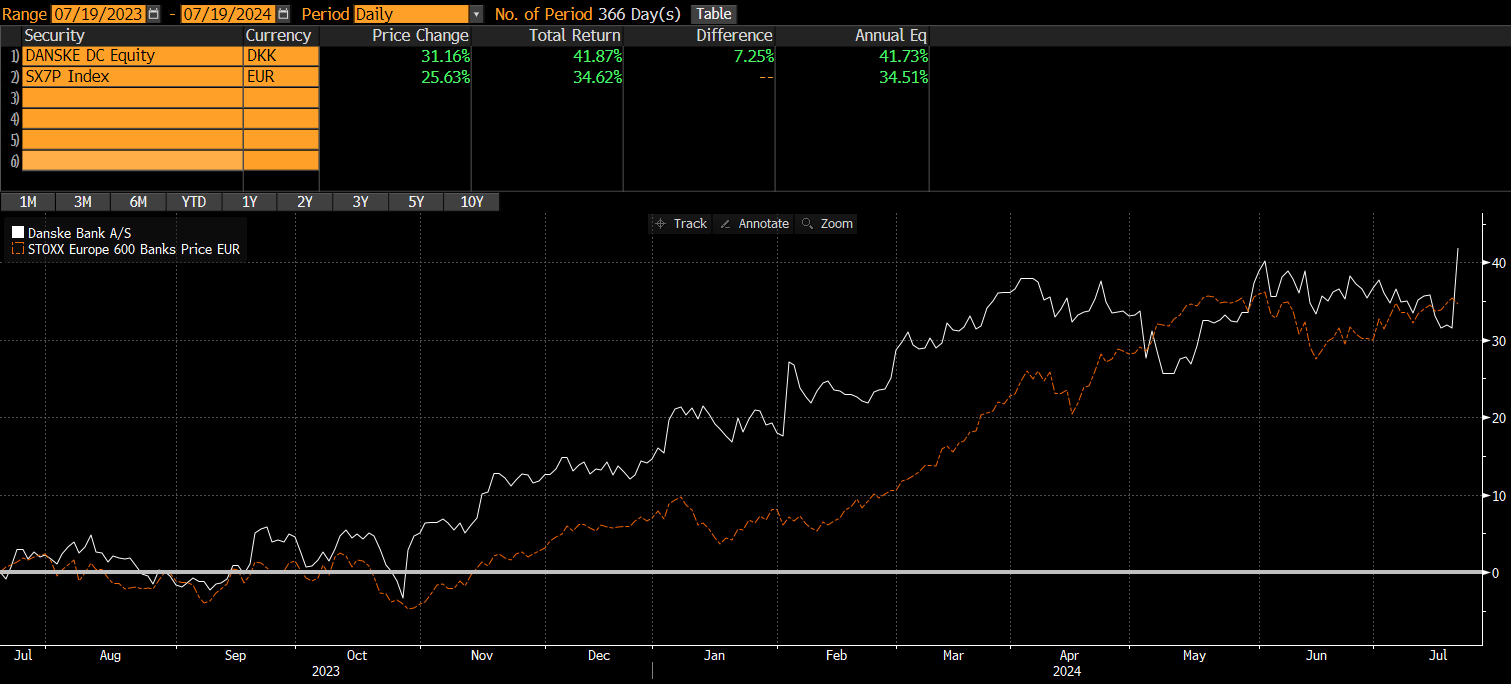

As I’ve lined in earlier articles, I see Danske as the most effective European banks and revenue play, as a result of its high-dividend yield that’s sustainable over the long run. Not surprisingly, its shares are up by greater than 40% over the previous 12 months, outperforming the European banking sector throughout the identical interval, as proven within the subsequent graph.

Share value (Bloomberg)

Because the financial institution has reported in the present day its Q2 2024 earnings, I believe it’s now time to investigate its most up-to-date monetary efficiency and replace its funding case, to see if it stays revenue choose within the European banking sector.

Danske’s Q2 2024 Earnings

Danske has reported its monetary figures associated to Q2 2024, beating market expectations each on the high and bottom-lines. On high of that, it additionally introduced greater capital returns than anticipated, resulting in a optimistic share value response with its shares up by greater than 7% on the day.

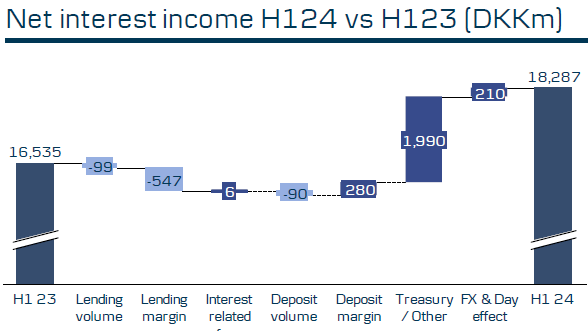

Throughout the first half of 2024, Danske continued to profit from the high-interest charge surroundings, resulting in a web curiosity revenue (NII) of almost $2.7 billion, up by 11% YoY. This optimistic efficiency was primarily supported by its treasury section, whereas lending quantity and decrease deposits had a slight destructive impression on the financial institution’s NII.

Internet curiosity revenue (Danske)

Within the first half of 2024, NII represented some 67% of complete revenues, which reveals that Danske has a major gearing to charges, although shouldn’t be among the many European banks extra uncovered, which normally have an NII contribution between 75-80% of complete revenues.

On condition that the European Central Financial institution has began to chop charges lately, which was adopted by the Danish central financial institution as a result of foreign money peg to the Euro, and the outlook is for additional cuts forward, this could result in NII headwinds within the coming quarters and, more than likely, Danske’s NII has most likely reached a peak in Q2 2024. Certainly, on a quarterly foundation, NII was flat supported by lending and deposit volumes, however going ahead its NII is predicted to say no as a result of decrease charges.

Regardless of that, its revenues are anticipated to keep up a optimistic trajectory within the coming quarters, being supported by greater payment revenue. Throughout the first half of this 12 months, its payment revenue amounted to greater than $1 billion, up by 13% YoY, justified by greater buyer exercise within the banking section and robust debt capital market efficiency. Internet revenue from the insurance coverage enterprise additionally carried out effectively, with clients transferring cash from deposits to financial savings merchandise.

The one income line that reported decrease revenues in H1 2024 was buying and selling revenue, which amounted to solely $200 million (-38% YoY), however Danske shouldn’t be a lot reliant on buying and selling revenue and the general impression on revenues was not a lot materials.

Attributable to greater NII and payment revenue, complete revenues elevated to greater than $4 billion in H1 2024, up by 9% YoY. For the total 12 months, the financial institution’s steerage is simply to develop revenues, which appears fairly conservative given its optimistic working momentum within the first semester, whereas the road expects revenues to be round $8.2 billion (+8% YoY).

Concerning prices, Danske reported working bills of $1.87 billion within the first semester of 2024, up by simply 1% YoY. That is fairly good contemplating the inflationary surroundings and wage progress strain in Denmark and throughout different Nordic nations, exhibiting that Danske was in a position to offset these pressures by decreasing prices elsewhere.

Its cost-to-income ratio was under 46% in H1 2024, under its mid-term goal of about 50%, which implies its effectivity is already fairly good, permitting the financial institution to proceed to put money into know-how and digitalization to enhance its effectivity within the close to future.

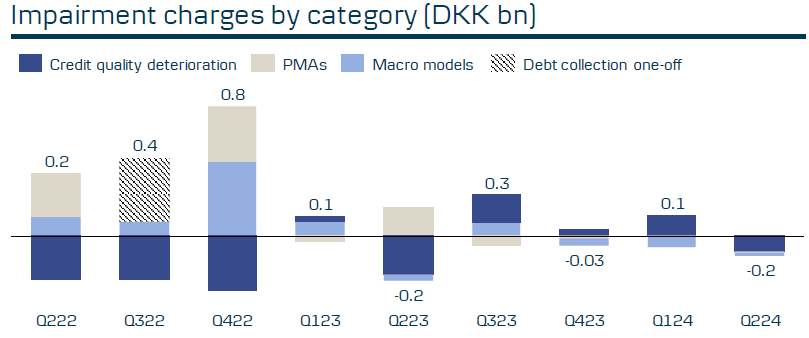

On the asset high quality facet, Danske has maintained a superior credit score high quality within the European banking sector and, regardless of greater charges lately, shoppers and company have maintained sturdy solvency ranges all through this era. Certainly, in H1 2024, Danske reported provision reversals of $14 million, exhibiting that credit score high quality throughout its mortgage e-book stays at very wholesome ranges.

Provisions for credit score losses (Danske)

For the total 12 months 2024, Danske’s steerage is for danger ranges to extend considerably as a result of macro and geopolitical uncertainties, anticipating danger provisioning to be about $87 million, which continues to be fairly low and isn’t anticipated to have a major impression on its earnings.

Attributable to greater revenues, good price management and resilient credit score high quality, Danske’s web revenue within the first semester of 2024 elevated by 13% YoY to greater than $1.6 billion and its return on fairness (ROE) ratio, a key measure of profitability within the banking sector, was 13.1%. For the total 12 months, its web revenue steerage was upgraded and is now anticipated to be between $3.1-3.3 billion, whereas beforehand Danske was anticipating a web revenue under $3 billion, exhibiting that its working momentum within the first half of the 12 months was higher than anticipated and the tempo of rate of interest cuts shall be doubtless moderated within the second half of this 12 months.

Concerning its capitalization, the financial institution has a really sturdy place on condition that its CET1 ratio was 18.5% on the finish of June, being the most effective capitalized banks in Europe. On condition that its aim is to have CET1 ratio above 16% by 2026, Danske has a major extra capital place and doesn’t have to retain a lot income forward, permitting to return important capital to shareholders over the subsequent few years.

Certainly, contemplating this sturdy capital place and the current settlement to promote its retail enterprise in Norway, which is predicted to shut till the top of 2024, Danske has loads of capital obtainable to return to shareholders.

This can be a important distinction from the earlier years, when uncertainty about its anti-money laundering (AML) points in Estonia and the price of settlements with totally different authorities and regulators led to small payouts to shareholders from 2018 to 2022. As this subject was settled in 2022, Danske is now in a unique section and might concentrate on capital returns as one in every of its most engaging options of its funding case.

Certainly, Danske shocked by saying an interim dividend to be paid within the coming days of DKK 7.50 ($1.09) per share, representing some 56% of its H1 2024 earnings. Buyers ought to notice that Danske has traditionally solely paid one dividend per 12 months, thus an interim dividend was not anticipated, exhibiting that Danske clearly has extra capital and doesn’t have to retain earnings.

Moreover, the financial institution additionally intends to distribute a particular dividend of about $800 million when the sale of its retail unit in Norway to Nordea (OTCQX:NRDBY) closes within the coming months, as there isn’t any want to spice up its capital ratio following this disposal.

Associated to its 2024 earnings, it needs to distribute the total remaining web revenue in 2025, whereas after that it’s going to once more resume an annual dividend frequency. Nonetheless, contemplating the financial institution’s sturdy place and natural capital era capability, there’s some chance that Danske can pay extra particular dividends or carry out share buybacks within the subsequent couple of years, enhancing its complete capital return coverage.

Based on analysts’ estimates, its complete dividend associated to 2024 earnings, not contemplating its ‘particular’ dividend associated to proceeds from the sale of its private clients enterprise in Norway, is predicted to be DKK 15.2 ($2.22) per share, representing a rise of 5% YoY. At its present share value, this results in a ahead dividend yield of round 7%, which is sort of engaging to revenue traders and is above the common of the European banking sector.

Concerning its valuation, Danske is presently buying and selling at 1.02x e-book worth, an analogous valuation in comparison with when I final analyzed the financial institution. Whereas this represents a premium to its historic valuation over the previous 5 years (0.7x e-book worth), traders ought to contemplate that as a result of its AML subject its valuation was fairly depressed in comparison with its fundamentals and has considerably re-rated for the reason that finish of 2022.

Regardless of that, in comparison with its Nordic friends, comparable to Nordea or Swedbank (OTCPK:SWDBY), Danske continues to commerce at a reduction on condition that its friends commerce, on common, at greater than 1.2x e-book worth. This low cost doesn’t appear to be justified, because the financial institution already has settled its historic points associated to AML, which implies its valuation appears to be engaging at present ranges.

Conclusion

Danske has reported a optimistic working efficiency within the first half of the 12 months and shocked the market with an interim dividend to be paid within the coming days, plus formidable plans to return extra capital to shareholders over the approaching 12 months. This clearly reveals that Danske can distribute a big a part of its earnings to shareholders sooner or later, making it dividend yield of seven% sustainable and fairly engaging to revenue traders. On high of that, its present valuation additionally appears to be undemanding, making Danske an attention-grabbing choose within the European banking sector.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.