Block: Great Firm At A Honest Worth (NYSE:SQ)

BlackJack3D/E+ through Getty Photographs

Funding thesis

I like firms which leverage sturdy ecosystems as this method creates sturdy cross-selling alternatives and will increase switching prices for patrons, a formidable combine to construct sustainable worth for shareholders. On this respect, Block, Inc. (NYSE:SQ) is a singular firm as a result of it leverages two ecosystems concurrently. This creates huge alternatives for the corporate to drive sturdy income progress for longer. The enterprise seems to be resilient to challenges and its broad diversification throughout completely different income streams can also be an indicator of power. The corporate is financially well-equipped to proceed investing in innovation and differentiation, which can seemingly assist in constructing a moat. My valuation evaluation means that the inventory is roughly pretty valued, which is a compelling alternative for such a stellar enterprise. Block is actually a “Robust Purchase” for me as a result of there’s a quote from the good Warren Buffett, which is one in all my most favorable ones.

It is higher to purchase an exquisite firm at a good value than a good firm at an exquisite value.

Firm data

Block offers cost and point-of-sale [POS] options to retailers within the U.S. and internationally.

The corporate’s fiscal 12 months ends on December 31 and there are two reportable segments: Sq. and Money App. Sq. combines software program, {hardware}, and monetary merchandise to serve retailers. Money App is an ecosystem of monetary services to serve customers.

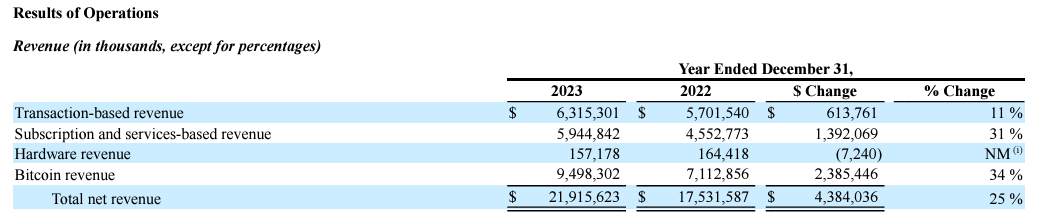

In response to the newest 10-Ok report, Money App is the most important section which contributed round 67% to the corporate’s complete income in FY 2023. It’s also very important to know the corporate’s income by sort, the place Bitcoin income is the most important one.

SQ’s newest 10-Ok report

Financials

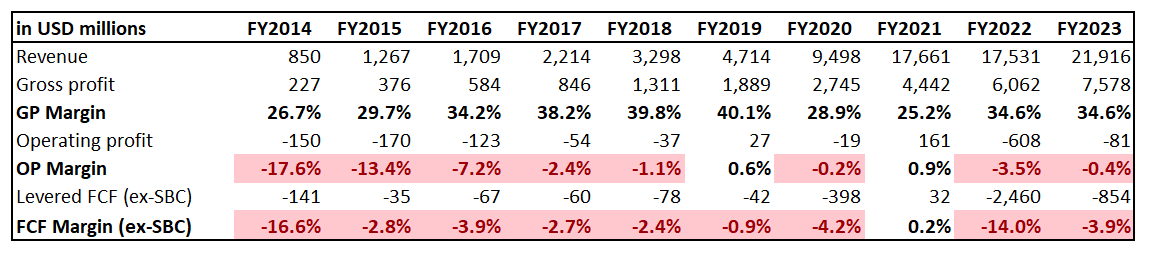

long-term tendencies in an organization’s efficiency provides me an understanding of how numbers mirror the effectivity and potential of the enterprise mannequin. During the last decade, Block’s income compounded with a staggering 44% CAGR.

Writer’s calculations

The essential issue is that the gross margin improved because the enterprise scaled up, indicating that the enterprise mannequin is economically sound, and the economies of scale impact is leverageable. The working and free money movement [FCF] margins additionally demonstrated optimistic dynamics earlier than the corporate notably boosted R&D spending beginning in 2021. The corporate invested $2.7 billion in R&D in FY 2023, which considerably weighed on the working and FCF margins.

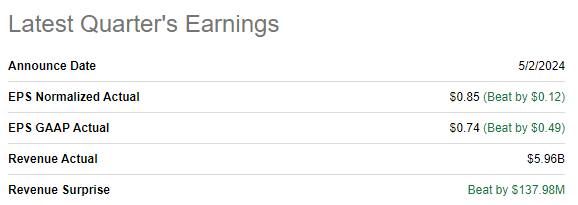

The newest quarterly earnings had been launched on Could 2, when the corporate topped each income and EPS consensus estimates. Income grew by 19.4% YoY and the adjusted EPS greater than doubled, from $0.40 to $0.85. The EPS power was ensured by the stable YoY working margin enchancment, from -0.12% to 4.19%. Block generated $900 million FCF in Q1, which represents a 15% FCF margin. The FCF margin seems to be stable even when the stock-based compensation [SBC] is deducted, roughly 10%.

In search of Alpha

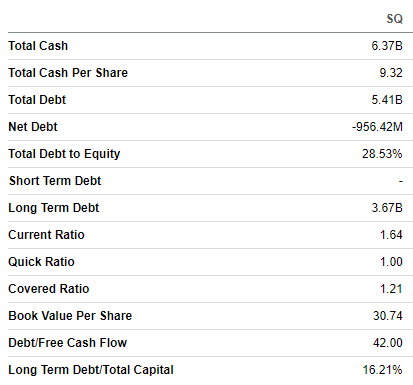

Regardless of having a close-to-zero FCF margin in recent times, Block’s stability sheet is strong with average leverage and internet money place. Liquidity metrics are additionally in fine condition, offering SQ with stable monetary flexibility to help its additional enlargement and innovation. Like many of the progress firms, SQ demonstrates progress within the variety of shares excellent. Nevertheless, the dilution doesn’t look dramatic as over the past two years the variety of shares excellent grew from round 580 million to 617 million as of the final reporting date.

In search of Alpha

As we see, the corporate demonstrates sturdy long-term tendencies in its monetary efficiency. Latest power additionally provides to my optimism however let me change to forward-looking insights now.

Block’s newest earnings presentation

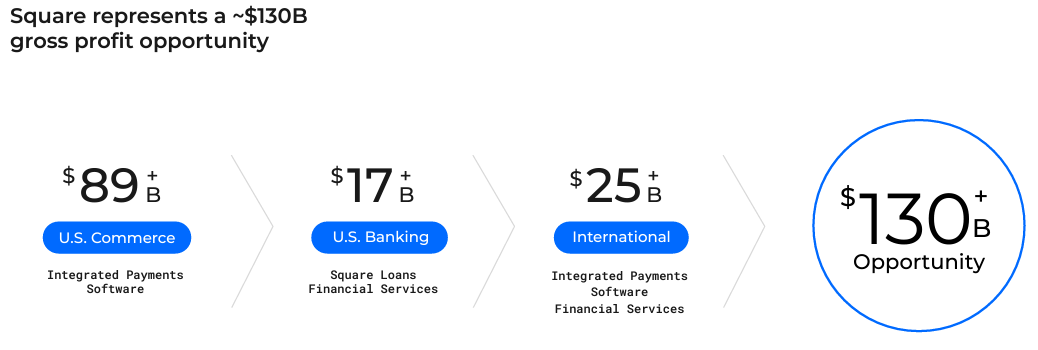

The addressable market is huge, as the corporate largely targets small and medium companies [SMB], which symbolize round 44% of the American economic system. The corporate sees an unlimited $130 billion gross revenue alternative, that means there’s nonetheless sturdy potential for progress.

fitsmallbusiness.com

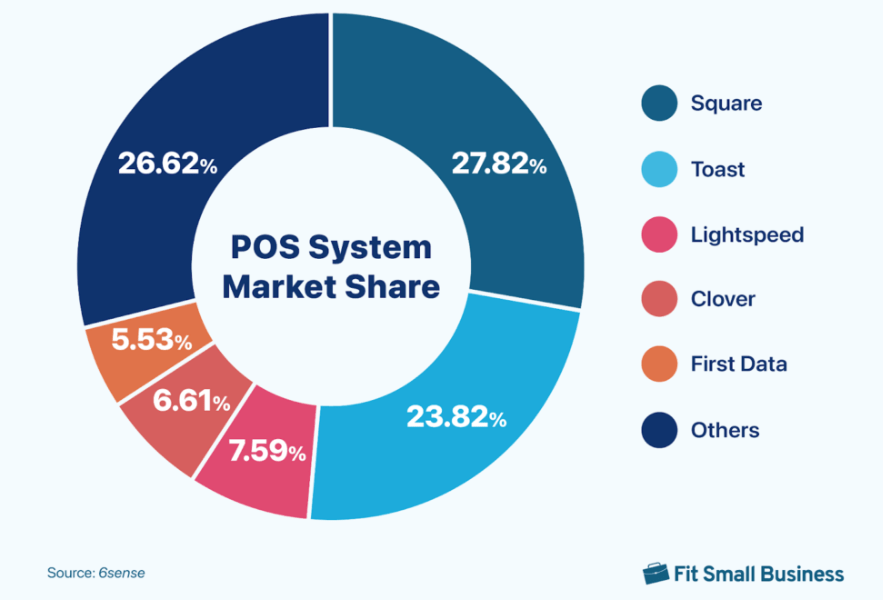

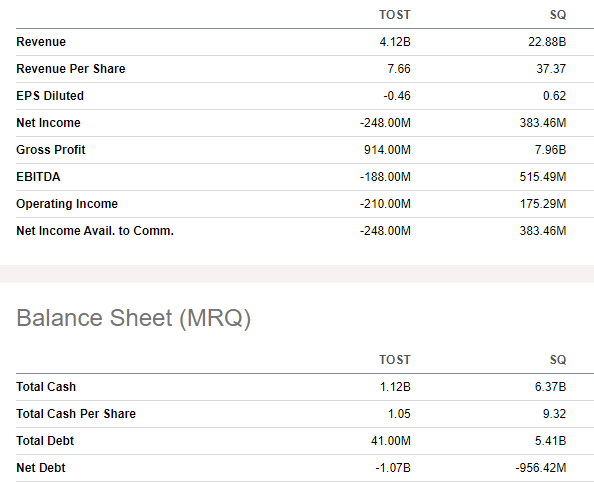

Block is in a stable market place with the most important, round 27%, market share within the POS market. Toast, Inc. (TOST) isn’t far behind with a 24% market share. Nevertheless, if we converse concerning the scale of the 2 firms, they’re incomparable. Block’s income is greater than 5 instances increased, and it has way more potential to reinvest and innovate. This makes Block higher outfitted to compete amongst these two firms.

In search of Alpha

Understanding of Block’s dominance within the cloud POS market is essential as a result of the trade is prospering. In response to Mordor Intelligence, the cloud POS market is projected to develop at a 24.2% CAGR. It is a sturdy tailwind, particularly contemplating Block’s main positions within the area of interest.

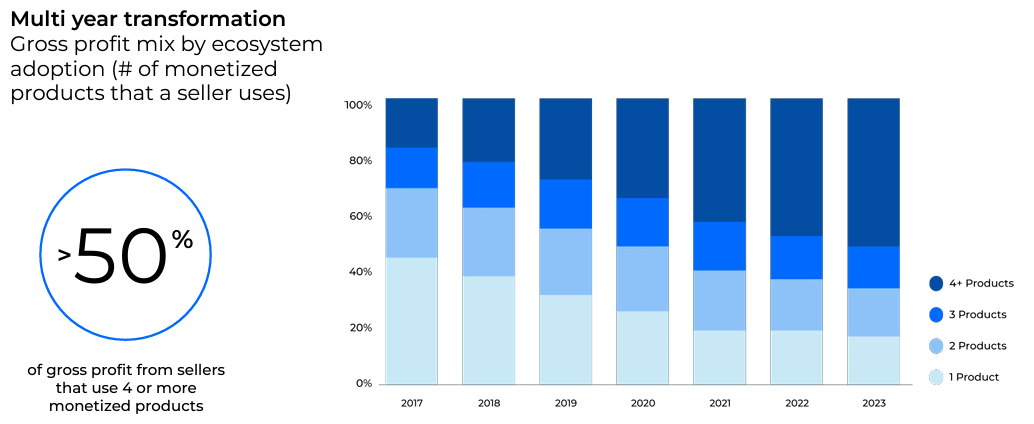

One other sturdy bullish signal is that every of the corporate’s segments represents a separate ecosystem. This allowed to considerably strengthen the corporate’s enterprise combine by way of cross-selling. The share of gross revenue generated from clients that adopted 4 or extra merchandise continues growing and already represents round 50%.

SQ’s newest earnings presentation

In my view, firms construct ecosystems to extend their cross-selling potential and enhance switching prices for patrons. The above bar chart means that SQ is kind of profitable in pursuing each these duties.

In response to the newest 10-Q report, Sq. generates round 94% of its revenues throughout the U.S. Quarterly worldwide income is under $400 million, that means there’s a sturdy worldwide enlargement alternative.

Final, however not least, aside from specializing in nurturing the highest line, the administration began prioritizing price effectivity as nicely. This means that the corporate is switching to a brand new section of its progress when high quality progress turns into extra essential than progress in any respect prices.

Total, I like Block’s enterprise mannequin which concurrently leverages two ecosystems, creating sturdy cross-selling potential. The market alternative is large, each domestically and internationally. The enterprise combine is nicely diversified throughout numerous income streams and finish markets, which makes the corporate’s monetary efficiency resilient. That is underscored by the truth that income didn’t dip throughout very difficult FY 2022, and the gross margin expanded throughout this turbulent 12 months.

Valuation

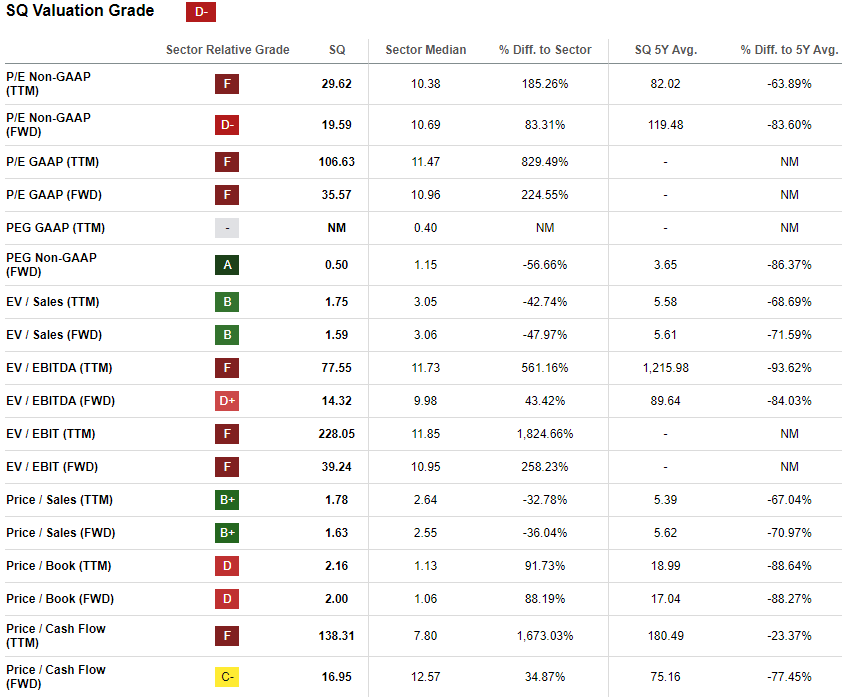

SQ at present trades a number of instances decrease in comparison with its 2021 highs achieved in the course of the pandemic-driven inventory market craze. Regardless of such a dip, valuation ratios are nonetheless extraordinarily excessive in comparison with the sector median. Then again, SQ is an organization that demonstrated a 44% income CAGR over the past decade and evaluating it to the sector median may not be appropriate.

In search of Alpha

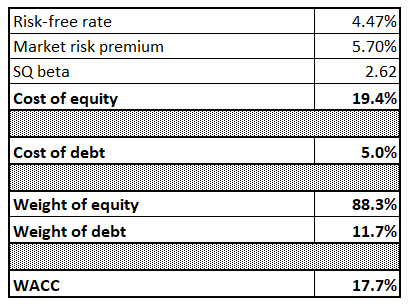

Since valuation ratios doesn’t assist a lot in Block’s case, I need to simulate the discounted money movement mannequin [DCF]. Assets which I normally depend on to acquire an organization’s WACC present very completely different suggestions for SQ. Due to this fact, I made a decision to calculate it on my own.

The chance-free price is 10-year Treasuries yield of 4.47% in the meanwhile. The market threat premium is final 12 months’s degree of 5.7%. In response to In search of Alpha, Block’s beta is 2.62. The load of debt isn’t important, so I apply a 5% rule of thumb for the price of debt. Tax defend additionally doesn’t apply for SQ as a consequence of losses. All in all, Block’s WACC is 17.7%.

Writer’s calculations

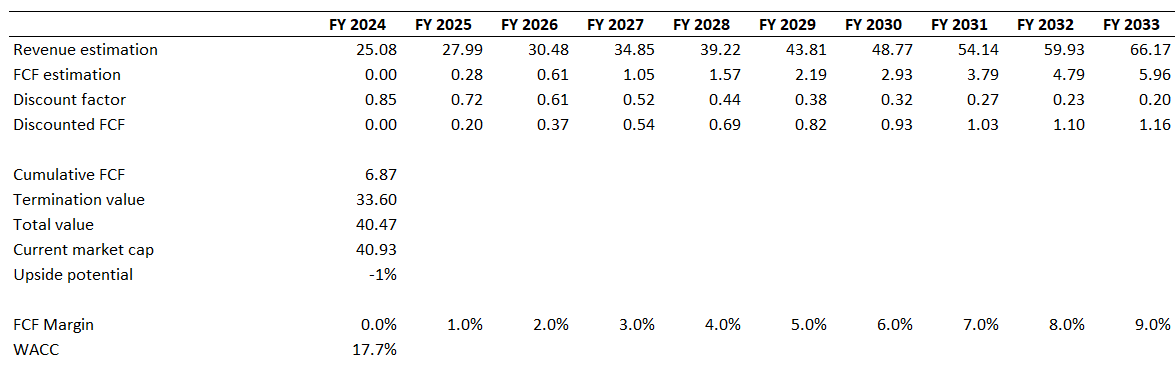

Counting on income consensus estimates proved to be a sound valuation technique for me. Furthermore, it doesn’t appear to be consensus estimates exaggerate income progress because the projected CAGR is 11%. Block’s FCF margin nonetheless dances round zero, which can be my estimate for the bottom 12 months. For the years past FY 2024, I challenge a one proportion level yearly enlargement in FCF.

Writer’s calculations

As proven above, SQ is sort of completely priced as a result of its present market cap could be very near the enterprise’s honest worth.

Dangers to contemplate

Because the addressable marketplace for SQ is important, it’s extremely seemingly that the competitors on this area will intensify. The competitors in digital funds is already fierce with a number of well-known manufacturers already within the sport like Apple Inc. (AAPL), Alphabet Inc. (GOOG), (GOOG), PayPal Holdings, Inc. (PYPL), Visa Inc. (V), and Mastercard Included (MA). Swiftly remodeling to adapt to altering shopper preferences can be an important side to endure the competitors. Differentiation from rivals requires substantial investments in R&D, which would require distinctive effectivity from the administration.

Worldwide enlargement is a stable progress alternative for SQ, however we even have to know that working internationally considerably will increase authorized and international change dangers. Furthermore, home success doesn’t assure that SQ will succeed internationally.

As an organization that handles monetary and different delicate buyer information, Block is topic to appreciable information privateness and cybersecurity dangers. Any information breach might erode the corporate’s repute, seemingly leading to litigation and monetary disruption.

Backside line

To conclude, Block is a “Robust Purchase”. It’s a fantastic firm with huge progress potential and sturdy resilience. The present share value is near the honest worth, which is a compelling alternative as a result of an organization like SQ actually deserves a premium to its share value.