Standing Of Banks’ Unrealized Losses In Q1 Worsened After Temporary Price Reduce Mania Aid

eternalcreative/iStock through Getty Photographs

Price-cut-mania soothed the ache, however it’s over.

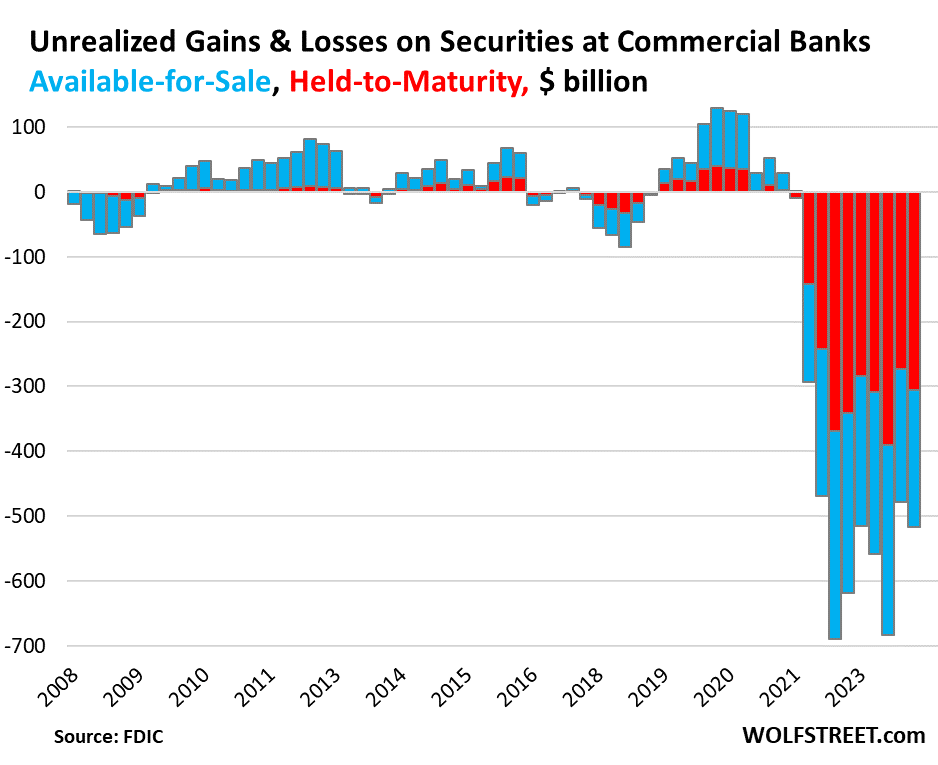

In Q1 2024, “unrealized losses” on securities held by industrial banks elevated by $39 billion (or by 8.1%) from This autumn to a cumulative lack of $517 billion. These unrealized losses quantity to 9.4% of the $5.47 trillion in securities held by these banks, in line with immediately’s FDIC’s quarterly financial institution knowledge for Q1.

The securities are principally Treasury securities and government-guaranteed MBS that do not produce credit score losses, in contrast to loans the place banks have been taking credit score losses, significantly in industrial actual property loans. These are pristine securities whose market worth dropped as a result of rates of interest rose. When these securities mature – or within the case of MBS, when pass-through principal funds are made – holders of those securities are paid face worth. However till then, increased yields imply decrease costs.

These unrealized losses had been unfold over securities accounted for underneath two strategies:

- Held to Maturity (HTM): +$31 billion in unrealized losses in Q1 from This autumn to a cumulative lack of $305 billion (pink).

- Out there for Sale (AFS): +$8 billion in unrealized losses in Q1 from This autumn to $211 billion (blue).

HTM securities (pink) are valued at amortized buy price, and losses in market worth do not hit revenue within the fairness portion of the stability sheet, however are famous individually as “unrealized losses.” It is with these HTM securities, and HTM accounting normally, the place the issues reside.

AFS securities (blue) are valued at market worth, and losses to due modifications in market worth are taken in opposition to revenue within the fairness part of the stability sheet.

Price-cut-mania soothed the ache, however it’s over

Yields on longer-term securities started plunging in November and bottomed out early this 12 months amid basic Price-Reduce Mania. The plunging yields precipitated costs to surge, which precipitated the unrealized losses in This autumn to drop from the large ranges in Q3.

However within the latter a part of Q1, Price-Reduce Mania started to subside, yields rose once more although not again to October ranges, and so the unrealized losses in Q1 rose as nicely.

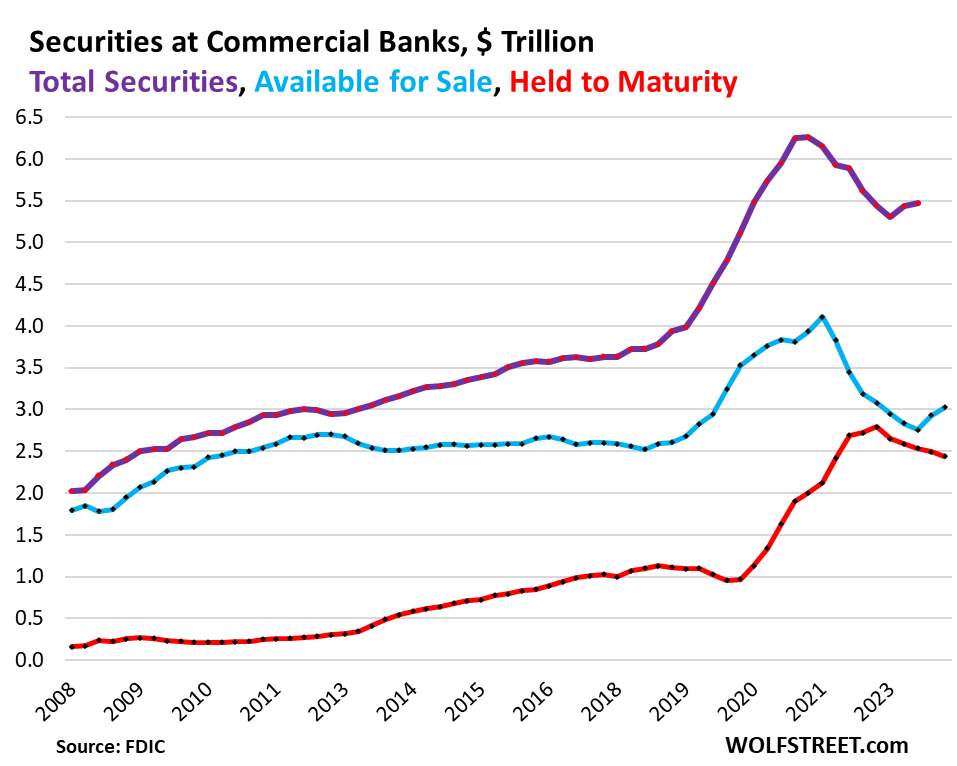

The $5.47 trillion in securities held by banks

Through the pandemic money-printing period, banks, flush with money from depositors, loaded up on securities to place this money to work, and so they loaded up totally on longer-term securities as a result of they nonetheless had a yield visibly above zero, in contrast to short-term Treasury payments which had been yielding zero or near zero and typically under zero on the time. Throughout that point, banks’ securities holdings soared by $2.5 trillion, or by 57%, to $6.2 trillion on the peak in Q1 2022.

That turned out to have been a colossal misjudgment of future rates of interest. The misjudgment already precipitated 4 regional banks – Silicon Valley Financial institution, Signature Financial institution, First Republic, and Silvergate Financial institution – to implode within the spring of 2023 when spooked depositors yanked their cash out.

In idea, “unrealized losses” on securities held by banks do not matter as a result of at maturity, banks will probably be paid face worth, and the unrealized loss diminishes because the safety nears its maturity date and goes to zero on the maturity date.

In actuality, they matter loads, as we noticed with the above 4 banks after depositors discovered what’s on their stability sheets and yanked their cash out, which pressured the banks to attempt to promote these securities, which might have pressured them to take these losses, at which level there wasn’t sufficient capital to soak up the losses, and the banks collapsed. Unrealized losses do not matter till they abruptly do.

The worth of securities held by banks ticked up in Q1 to $5.47 trillion, after having already ticked up in This autumn, however remains to be down by $786 billion, or by 12.6%, from the height in Q1 (purple within the chart under).

HTM securities have declined steadily from the height in This autumn 2022, and dipped additional in Q1, to $2.44 trillion, down 12.7% from the height (pink).

AFS securities rose for the second quarter in a row to $3.02 trillion however stay 26.4% under the height in Q1 2022 (blue).

A number of components make up the decline of securities on financial institution stability sheets from the height, together with:

- The portion of securities of the collapsed banks that the FDIC bought to non-banks is now not a part of it.

- Banks have written down AFS securities to market worth.

- Some securities matured.

- Banks might have bought some securities.

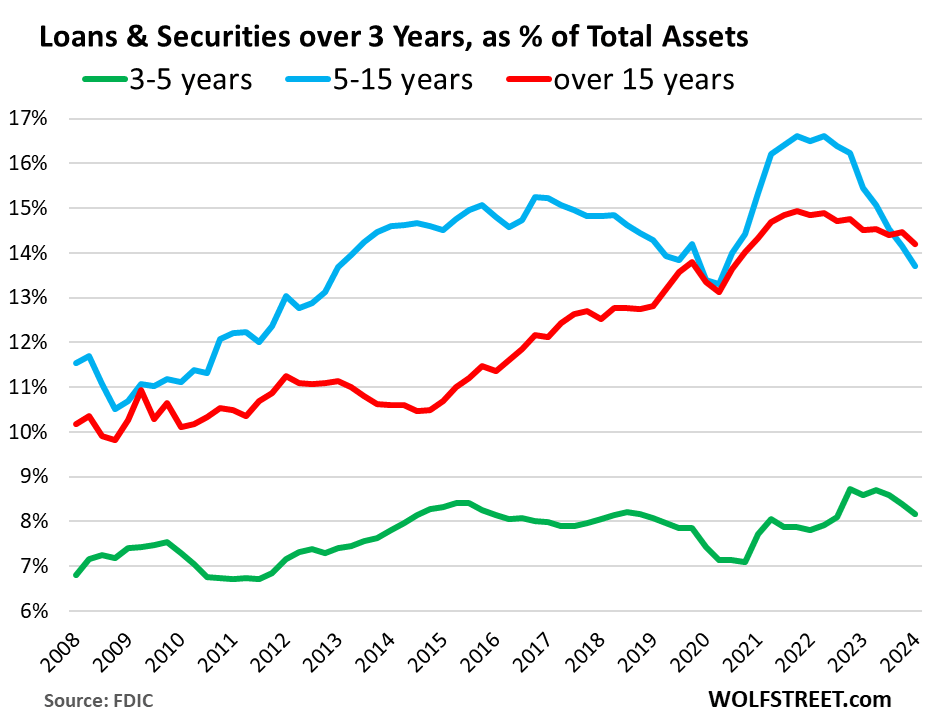

The longer until maturity, the larger the rate of interest threat

Rate of interest threat – the chance of falling costs as yields rise – will increase with the time period of the safety or mortgage. The 30-year Treasury securities bought in the summertime of 2020 have misplaced probably the most in market worth, whereas 5-year Treasury securities bought on the similar time are actually only a 12 months from maturing and are buying and selling at small losses from face worth.

To gauge this threat on financial institution stability sheets, the FDIC gives knowledge on securities and loans by remaining maturity:

- Least dangerous (inexperienced): 3-5 years: 8.2% of whole belongings.

- Riskier (blue): 5-15 years: 13.7% of whole belongings, lowest since Q2 2020, after substantial declines.

- Riskiest (pink): 15+ years: 14.2% of whole belongings, lowest since Q2 2020.

Editor’s Be aware: The abstract bullets for this text had been chosen by Looking for Alpha editors.